Markets & Economy

Categories

Market Volatility

Renewed volatility means it’s time to refocus on fixed income

Mike Gitlin

Mike Gitlin

February 12, 2018

KEY TAKEAWAYS

- Prospects for higher U.S. inflation appear well supported.

- Yield-chasing bond strategies can leave investors more vulnerable to further selloffs in equities.

- Investors should seek to upgrade their portfolios.

Mike Gitlin, head of fixed income at Capital Group, has 24 years of investment industry experience. He discusses the current market environment and what it means for bond investors.

Volatility appears to have been sparked by concern that much higher bond yields are on the horizon. What’s your take?

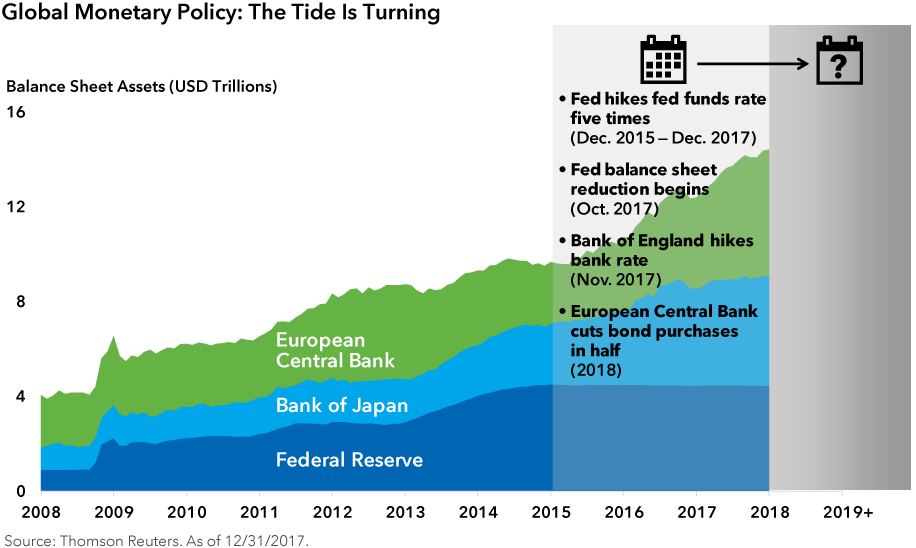

The turning tide of global central bank monetary policy has, in my view, played a critical role. Developed market central banks were incredibly accommodative for nearly a decade, providing a tailwind to asset prices.

Now, policy is tightening. The Federal Reserve raised interest rates five times since December 2015, and is shrinking its balance sheet. The Bank of England hiked for the first time in a decade in November 2017. The Bank of Canada has raised rates three times since July 2017, and the European Central Bank is committed to reducing asset purchases.

“Don’t bet against the Fed,” goes the old adage. How much of a headwind will assets face amid less supportive policy? That’s the big question that is buffeting markets, and we’re considering it carefully.

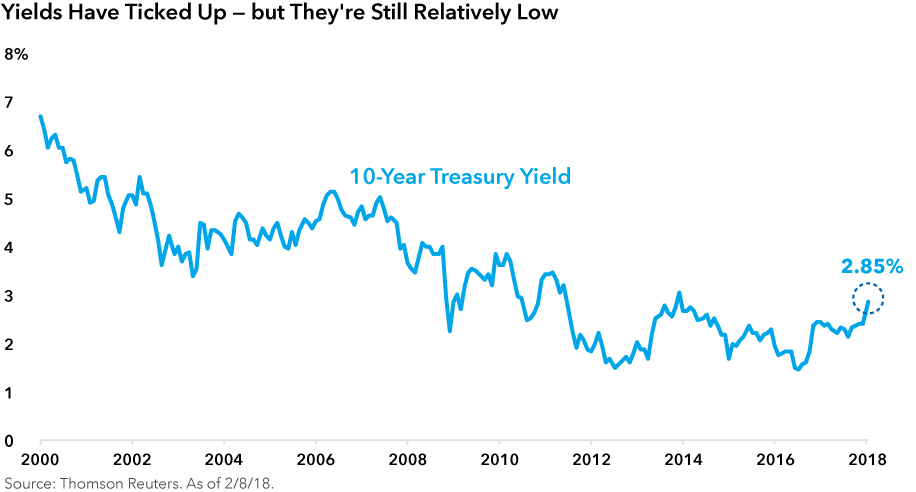

Certainly volatility can feel unsettling, so it’s doubly important for investors to keep things in perspective. The 10-year U.S. Treasury yield was 2.85% as of February 8, 2018. This is less than a quarter percentage point higher than the level a year earlier. And a year from now, the yield could be another quarter of a percentage point higher, according to forward markets — hardly a dramatic move.

Higher longer term bond yields have often signaled a coming upturn in inflation. What’s your outlook for U.S. inflation?

Our interest rates team thinks core inflation could reach 2.4% in 2018 — if solid wage gains continue. Productivity growth was -0.1% for the fourth quarter of 2017. If productivity remains anemic, increased labor costs will need to be borne by companies and consumers.

We are also monitoring unemployment. Analysis by our economists suggests falling unemployment could also feed through into core inflation. A decline in the unemployment rate from 4.1% to 3.5%, for instance, could push annualized wage growth a quarter of a percentage point higher.

You’ve recently talked about the need for investors to also be mindful of credit risk in the current environment — why is that?

Credit markets are, according to various measures, somewhere between fair value and full value, and certainly not cheap. Investor demand has pushed down yields on corporate bonds. Their yield gaps (or, spreads) to Treasuries have approached record tight levels.

Fundamentals for the companies issuing these bonds remain broadly supportive. Even so, it wouldn’t be surprising to see credit spreads widen back out from here.

The hunt for yield has led some bond strategies to increase their investments in credit, including high-yield corporates. This could pose a particular challenge right now because high yield tends to be highly correlated with equities. Put differently, some core bond strategies may not provide the diversification from equities that investors expect. That could be a problem.

How widespread is scope creep among bond strategies?

Many bond funds appear to have strayed from their original missions in the low-interest-rate environment of the past decade.

To dig deeper, we conducted our own simple study centered on Morningstar’s short-term bond category. This is a category that should be all about capital preservation and diversification from equities.

We focused on funds that notched top-quartile annualized returns for the three years ended December 31, 2017. We found that the majority of funds that fared exceptionally well had also taken significant risks.

Indeed, many seemed to behave more like credit funds, not the kind of conservative fund that a retiree might choose as a reasonable yield enhancement over money market funds.

So, some bond strategies have been overly focused on finding yield, what should investors be looking to achieve with their fixed income?

Many bond funds may be taking more risk than their clients are aware of. It’s important that investors refocus on the four primary roles of fixed income in a balanced portfolio: diversification from equities, income, inflation protection and capital preservation.

That is exactly how we use fixed income in our target date funds, and it’s how we think advisors should think about bond portfolios for their clients. For most investors, maintaining a long-term perspective is a critical step towards achieving their goals. This means maintaining an appropriate balance of equities and fixed income through volatile periods.

That said, the current pullback may present a great opportunity for investors to upgrade their bond portfolios to what we refer to as true core: that means reallocating to bond funds that offer the potential for both solid income and diversification from equities.

Learn more about

Past results are not predictive of results in future periods.

The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings.

Higher yielding, higher risk bonds can fluctuate in price more than investment-grade bonds, so investors should maintain a long-term perspective.

© 2018 Morningstar®, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. These numbers were calculated by Capital Group based on underlying Morningstar data.

Our latest insights

-

-

-

Market Volatility

-

Market Volatility

-

World Markets Review

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.