Markets & Economy

Categories

Technology & Innovation

Where’s all the volatility in tech stocks?

Irfan Furniturewala

Irfan Furniturewala

Mark Casey

Mark Casey

August 23, 2017

Technology stocks have long been thought of as high beta, or more prone to sharp price swings than, say, a consumer staples or utilities company. Not so much anymore: Technology stocks are currently among the least volatile in the S&P 500 and are experiencing an influx of broad-based buying by a cross-section of investors. Growth funds, hedge funds, momentum strategies and multi-asset strategies have been drawn to technology stocks for their higher growth rates, visibility of earnings, strong balance sheets and dominance in their industries.

There’s no doubt market volatility has declined broadly as stocks have climbed steadily for the past 17 months, supported by central bank-induced liquidity, an improving global economy and earnings growth. But this can reverse quickly in a market correction.

So why is volatility so low now? Here, portfolio managers and analysts at Capital Group weigh in:

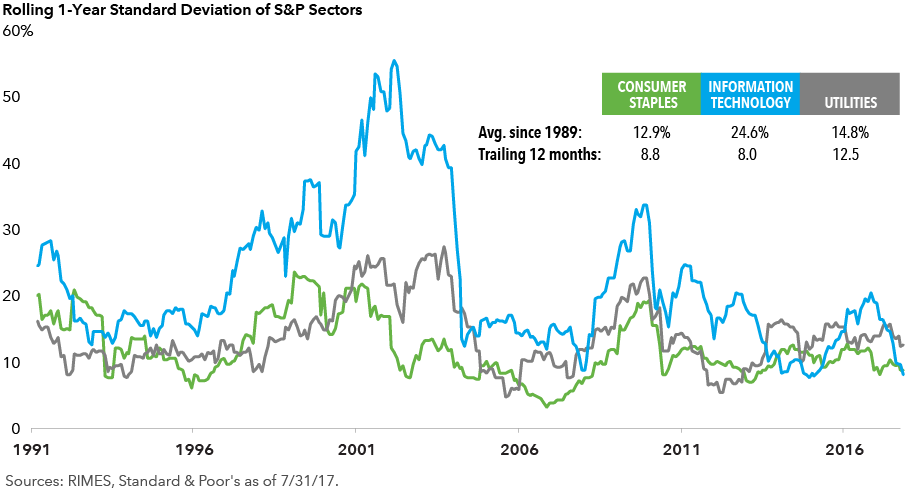

The new “Steady-Eddy” world of tech shares

Technology companies have been known for their innovations and for the lofty expectations placed on them, making the sector traditionally one of the most volatile on the stock market. Now, in a sign of the sector’s maturation, tech shares are trading like defensive consumer staples and utilities — the least volatile sectors going back to 1989. Furthermore, their products have become more of a utilitarian-like service than a discretionary item.

“There is so much comfort around the dominance of the large technology companies that there is a sense these companies are becoming the new consumer staples, given the consistency of their businesses and how ingrained their products are in our daily lives,” says investment analyst Irfan Furniturewala, who covers U.S. hardware and semiconductor companies at Capital Group. “A 22-year-old who has just started work would rather pay up for a high-speed internet connection and a smartphone as opposed to leasing a car. It’s one of the reasons why I see Netflix and Amazon Prime as compelling value propositions.”

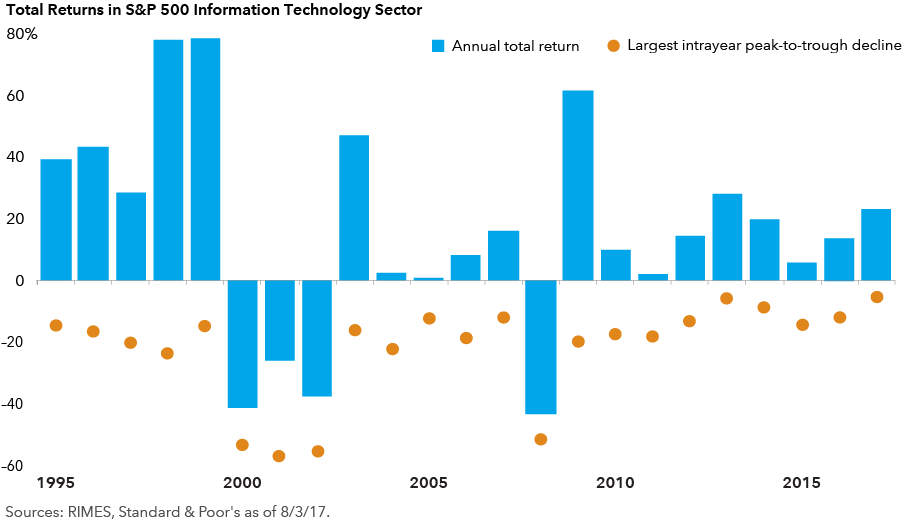

Tech stocks positive 18 of past 22 years

Nevertheless, technology stocks can swing from gains to losses during the course of a year. Given the potential for above-average growth compared to other industry sectors, investor expectations can run high. This means quarterly earnings reports are closely watched, making any slip-ups costly in terms of resulting stock prices.

For investors prepared to handle short-term selloffs, taking a long-term approach has had its benefits.

In 18 of the past 22 years, technology stocks have risen. Put another way, even when the S&P 500 Information Technology sector declined by double-digits within a given year, it managed to finish that calendar year in positive territory 80% of the time.

“Investor sentiment can fluctuate, and these large U.S. technology companies will likely be subject to short-term noise that will affect their share prices. But for the most part, I believe Amazon, Alphabet and Facebook continue to have very long runways for growth,” says portfolio manager Mark Casey, who covers U.S. internet companies at Capital Group. “I know it’s not common for companies with market caps as big as these to grow at healthy rates and to keep amassing market cap. That said, it’s also not common for companies to have user bases well in excess of one billion per month. Google has several products with over a billion users, while Facebook has three. Furthermore, it’s also not common for companies to succeed on a global basis so quickly nor to have so many ways to make money.”

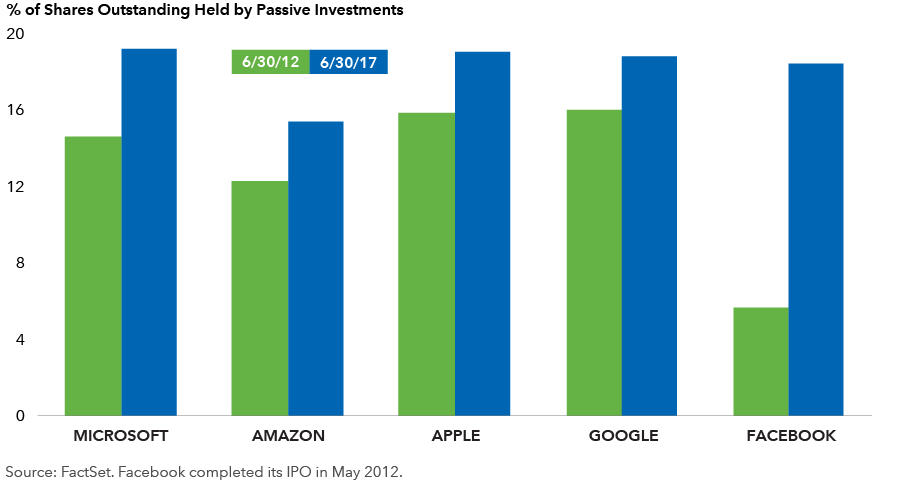

Passive holdings in tech stocks have increased

Mega-cap tech stocks are being added to more and more passive index products that have very different investment objectives. Apple, Alphabet and Microsoft are currently held in a number of low-volatility and momentum offerings, according to a recent Wall Street Journal article.

Another key change from a few years ago is the low dispersion of returns among big technology stocks.

The share price movements of Facebook, Amazon and Alphabet have become highly correlated over the last 52 weeks, according to Capital Group research. This trading pattern has emerged even though each company has different business fundamentals and operates in different segments of the technology industry.

“Historically, company share prices would move on company-specific news. Now, at certain times, it seems as if technology companies are being bought or sold together based on a particular group characteristic rather than on individual company fundamentals. Part of the reason is the ownership of technology by sector funds, momentum funds and quantitative strategies,” says Larry Solomon, a portfolio manager for The Growth Fund of America.

“In this current environment,” Solomon adds, “I’m seeking to mitigate downside risk through rigorous company-by-company analysis and identifying those sell candidates where I have less conviction in my original investment thesis or where the stock has reached my price target. This approach will give me more flexibility if the market turn lowers. As this bull market runs its course, being very disciplined about which stocks we continue to hold becomes ever more important.”

Learn more about

Past results are not predictive of results in future periods.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2018 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

Our latest insights

-

-

-

Market Volatility

-

Market Volatility

-

World Markets Review

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.