Artificial Intelligence

Categories

Chart in Focus

Are China’s tech giants making a comeback?

Kent Chan

Kent Chan

March 18, 2025

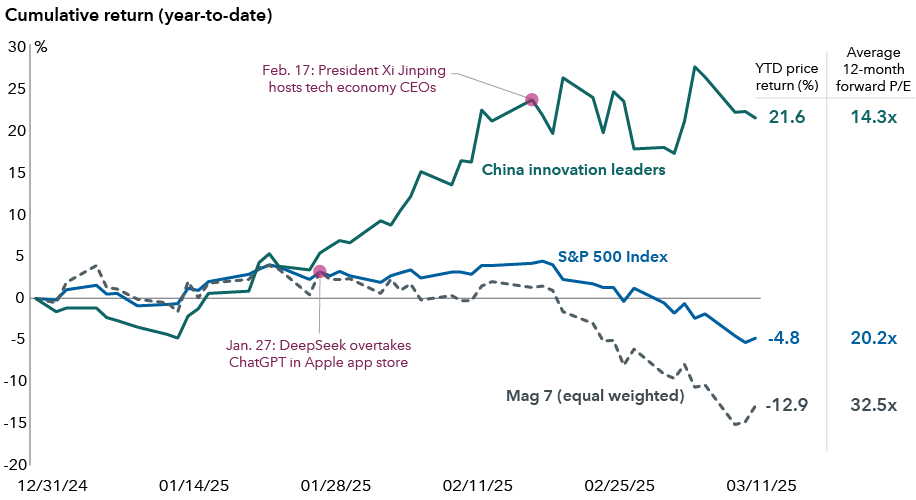

Here’s a recent event that would have been almost unthinkable a few years ago: China’s President Xi Jinping and top party leaders hosted a meeting with the country’s most prominent entrepreneurs. The message: It’s time for the private sector to make its mark.

The meeting came soon after China startup DeepSeek shocked global markets with its artificial intelligence (AI) training model, shifting the narrative away from the U.S. leading the AI race.

The MSCI China Index has led major global equity benchmarks this year, rallying 18% as of March 12, fueled by gains in information technology and consumer discretionary sectors. As the chart shows, China’s innovators have outpaced their Magnificent 7 (Mag 7) counterparts and the broader S&P 500 Index.

China's tech leaders pull away from the Mag 7

Source: FactSet. P/E = price-to-earnings. Mag 7 = Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. China innovation leaders = Alibaba, BYD, JD.com, Meituan, NetEase, PDD Holdings and Trip.com. Data from December 31, 2024, to March 12, 2025. P/E ratios for Mag 7 and China innovation leaders reflect average P/E ratios across listed companies. The P/E ratio for the S&P 500 Index is market-cap weighted.

Will the gains hold? It’s uncertain given China’s historically volatile stock market. Recent developments underscore China’s policy cycle is moving in a more positive direction. The government has become more vocal in its support of innovative private companies. That’s a shift from late 2020 to 2021, when the private sector faced regulatory scrutiny, sparking a broad sell-off and a crisis of confidence among entrepreneurs, domestic consumers and investors.

The sharp move up for the MSCI China Index is also reminder that innovation is global and select growth opportunities can be discovered in non-U.S. markets.

Going forward, potential gains for China’s equity market are likely to be more differentiated, as investors gauge which companies will see greater earnings revisions. Our investment analysts, for instance, don’t think certain internet platform companies are expensive, even after the rally, due to the potential for better margins and re-accelerating revenue.

Consensus expects 8% earnings growth for the MSCI China Index in 2025, led by areas within technology and consumer industries, based on FactSet estimates as of March 6. The risk is that profit projections get revised lower — a pattern we’ve seen in recent years due to China’s economic slowdown and lack of big-bang stimulus the market has hoped for.

There are also downside risks to economic growth. Fresh U.S. tariffs on Chinese goods and technology-related sanctions could weigh on certain companies. Domestic consumption also remains subdued. And while home sales in large cities picked up in January and February, the ailing property market is far from healed.

Learn more about

Past results are not predictive of results in future periods.

The S&P 500 Index is a market-capitalization-weighted index based on the results of approximately 500 widely held common stocks.

The MSCI China Index captures large- and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs).

Don't miss our latest insights.

Our latest insights

-

-

Health Care

-

Market Volatility

-

Market Volatility

-

Chart in Focus

RELATED INSIGHTS

-

Artificial Intelligence

-

Artificial Intelligence

-

Health Care

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility. These risks may be heightened in connection with investments in developing countries.

Investing in developing markets may be subject to additional risks, such as significant currency and price fluctuations, political instability, differing securities regulations and periods of illiquidity, which are detailed in the fund's prospectus. Investments in developing markets have been more volatile than investments in developed markets, reflecting the greater uncertainties of investing in less established economies. Individuals investing in developing markets should have a long-term perspective and be able to tolerate potentially sharp declines in the value of their investments.

The indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

Each S&P Index ("Index") shown is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.