U.S. Equities

Categories

India

What India's election means for financial markets

Nicholas J. Grace

Nicholas J. Grace

May 8, 2019

Financial markets are anxiously awaiting the final outcome of India's five-week general election. Official results won’t be known until May 23, and the big unknown is: Can Prime Minister Narendra Modi and his BJP party win enough votes to maintain their legislative majority and empower them to continue pursuing pro-business reforms?

The result will impact emerging markets sentiment. Modi won a decisive victory five years ago, and he’s taken some strides to improve India’s business climate.

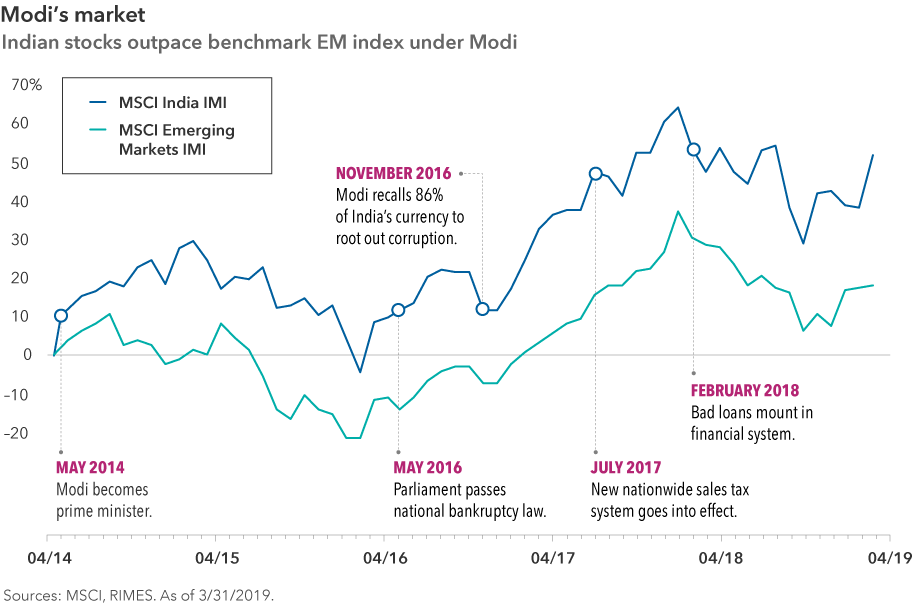

While Modi has not realized all of his lofty expectations as of yet, investors have acknowledged the progress: Indian stocks have widely outpaced the benchmark emerging markets index since May 2014 despite uneven economic growth and oil-price swings that resulted in bouts of volatility.

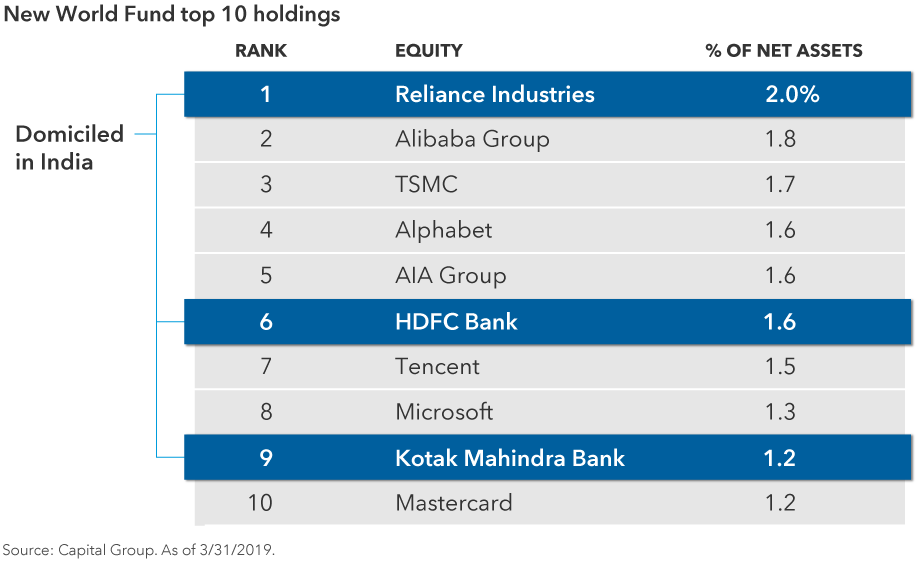

Fresh from a recent trip to India, portfolio manager Nick Grace, co-principal investment officer of New World Fund®, spoke to us about potential disruption in India’s retail sector and the impact of Modi’s reforms. The fund owns three Indian stocks among its top 10 holdings.

What does this election mean for India and its equity markets?

India is on the cusp of major changes, and it’s important to maintain the reform momentum that’s been established. I commend Modi for what’s he’s done. He’s ushered in a bankruptcy law that’s forcing banks to recognize bad loans more quickly and a national sales tax that replaced an inefficient web of state taxes.

There’s also been some backlash. Modi’s abrupt move to cancel 86% of the country’s currency in November 2016 was deeply unpopular. But he wanted to tackle corruption to improve the long-term health of doing business in India and increase the country’s tax revenue base.

In this election, it’s certainly possible Modi won’t have the same backing to push for sweeping change that he had when he became prime minister. That said, we continue to have strong convictions in our top Indian holdings, which include Reliance Industries, HDFC Bank and Kotak Mahindra Bank.

There are several possible outcomes to this election.

- Modi wins and the BJP retains a healthy majority in the legislature; this is my base case, and I believe this would be the best possible outcome for markets.

- Modi wins a narrow majority or is forced to form a coalition government to retain power, which would likely further slow his deregulation agenda.

- Modi and the BJP are defeated.

Ultimately, investors should be braced for some volatility if his power is weakened. Right now, markets appear to be pricing in a Modi win.

How have you been navigating this landscape in New World Fund?

Investing in cyclical companies has been a challenge given economic disruptions and periods of higher oil prices, which have made cement and auto companies less appealing. And many consumer-related stocks are expensive.

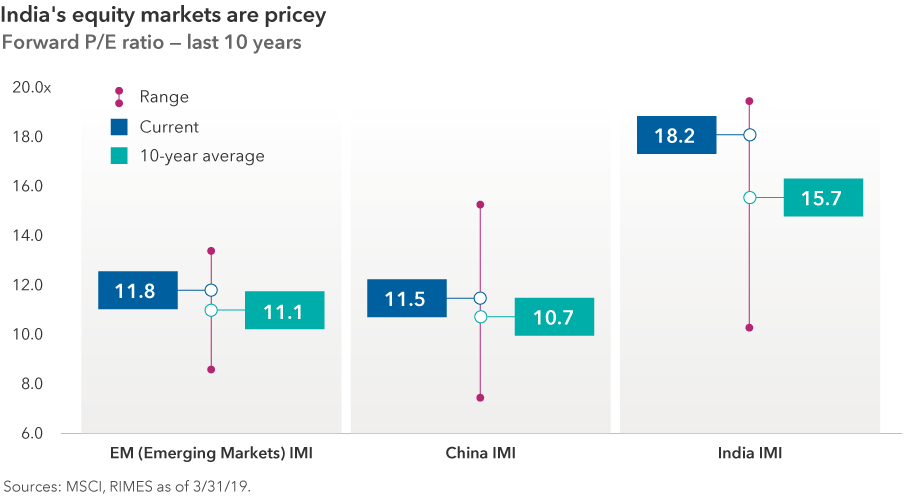

Overall, valuations for Indian stocks are demanding. They trade at 18.2 times forward earnings in aggregate, which is pricey compared to a multiple of 11.8 times for the benchmark MSCI Emerging Markets Investable Market Index.

That’s why I’m focused on companies that I believe have specific growth drivers that would be unaffected by what results from the election.

Conglomerate Reliance Industries is one of those companies. It upended India’s telecom sector when it launched its Jio mobile service in 2016. Jio now has one of India’s largest subscriber bases at 306 million, and the industry has consolidated with its emergence, leaving it as a dominant player in a country where mobile phone usage is projected to expand significantly.

Reliance is now looking to leverage its capabilities to build a mobile platform that connects manufacturers to retailers and consumers. While still in the very early stages, this initiative may lead to some promising growth opportunities.

Amazon and Walmart are investing billions of dollars in India. What does this mean for the retail sector and e-commerce?

I believe we will see a shift in how the retail industry is operated and structured.

The country is becoming a battleground for powerful multinationals and homegrown Indian companies, and the government has been pursuing e-commerce regulations to help protect local businesses and Indian consumers. But I think there will be a limit to how much they push. Modi has been an advocate of a “digital India,” and U.S.-led investments to sell to Indian consumers have been substantial.

Amazon has pledged to invest roughly $5 billion. Last year Walmart paid $16 billion for a majority stake in Flipkart, an upstart Indian e-commerce platform.

At a high level, the country’s retail market (very broadly defined to include everything from groceries to jewelry to apparel) is valued at roughly $800 billion today, with the bulk of that in traditional retail channels like neighborhood stores and produce markets, based on our data.

Companies like Amazon, Walmart and Reliance are all pursuing strategies that could ultimately restructure traditional distribution channels in India, reshaping how household staples and other items get from manufacturing plants to neighborhood stores.

This could translate into lower prices, more efficient supply chains and less waste — especially for food products. In theory, this could help curb inflation in India (historically an issue) and keep interest rates lower.

The financial sector has faced credit quality issues over the past several years. What’s your outlook for banks?

Our investment analysts in New World Fund remain positive on a few private sector banks, namely HDFC and Kotak Mahindra. These banks have grown rapidly over the past decade. They have top-notch management teams and quality loan underwriting standards. With loan issues bogging down some of the state-run banks and non-bank lenders, they should continue to gain market share.

The new bankruptcy law should strengthen the credit system and corporate governance. So far, it appears to be progressing well. Based on data we’ve seen, the average time to resolve a bad debt issue shrunk markedly to 310 days, with an average recovery rate of 49%. That compares with an average of 10 years and 22% recovery rate before the law took effect.

This bodes well for the banking sector and India’s economy.

Learn more about

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Our latest insights

-

-

Global Equities

-

Economic Indicators

-

-

RELATED INSIGHTS

-

Asset Allocation

-

Global Equities

-

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.