Market Volatility

Categories

Taxes

Tax-aware investors should rethink high yield

Greg Ortman

Greg Ortman

February 21, 2018

KEY TAKEAWAYS

- Caution regarding high-yield corporates seems appropriate.

- High-income municipal bonds could be a good alternative.

- They typically have low equity correlation and higher credit quality.

- The opportunity set is large and varied.

High-yield corporate bonds have been on a tear. Total returns in January were 0.6%, building on a gain of nearly 8% in 2017 for the Bloomberg Barclays U.S. High Yield Index. For many investors seeking higher income and total returns, this fixed income asset class has been the place to be.

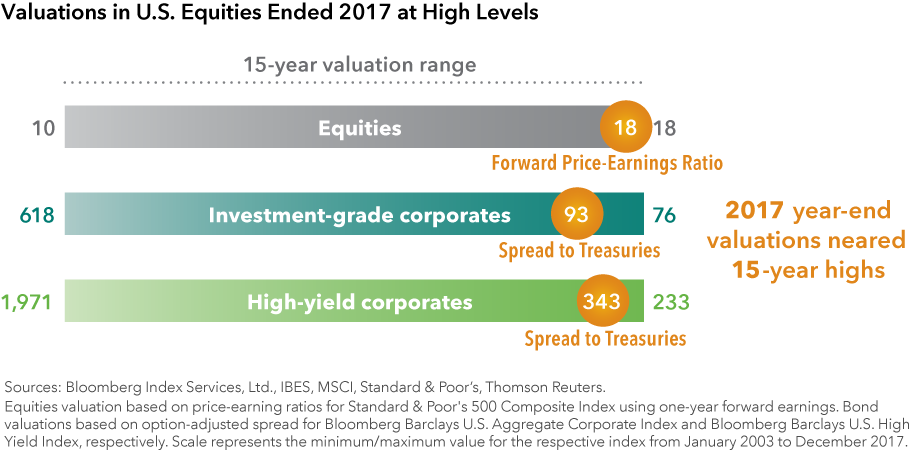

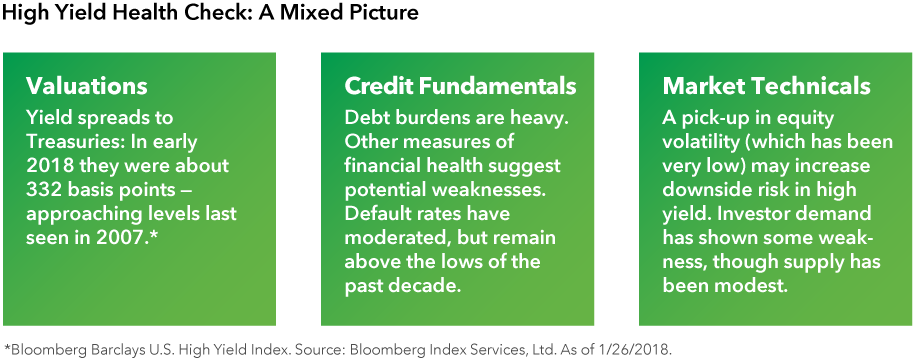

Following an extended rally, however, high-yield valuations have begun to look stretched. This is true for credit broadly, which would also include both U.S. investment-grade corporates and equities.

As Harry Phinney explained in January, the potential for significant additional yield spread tightening and price appreciation in the high-yield corporate bond market appears to be limited.

And while there have been few signs that a major turn for the worse is imminent, now seems like an appropriate time to consider alternatives to high yield.

High yield has had a good run, but is running out of track

Seasoned high-yield investors may sense that valuations feel rich. In order to target a similar level of income to that offered several years ago, investors have generally had to accept greater credit risk.

Given the current combination of valuations and fundamentals, caution seems appropriate. And for investors with equity-heavy portfolios, there's another potential pitfall: The asset class has tended to be highly correlated with equities.

In other words, if stocks sink, they’re likely to take high yield down with them.

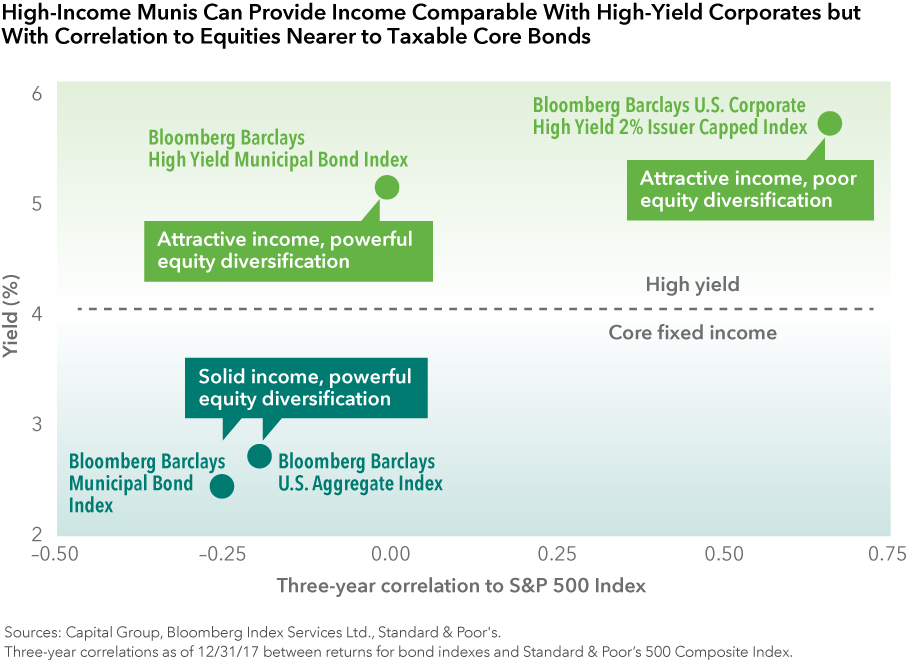

Reasons to consider reallocating from taxables to municipals

Higher income municipal bonds offer comparable yields to their taxable counterparts — in excess of 5%. And when the potential tax advantage is factored in, the income opportunity in municipals becomes even harder to ignore.

In the post-tax reform world, the after-tax income potential of municipals still outshines comparable taxable bonds. To calculate the taxable equivalent yield for investors in the highest income tax bracket, we’ll assume a federal marginal tax rate of 37% (the top 2018 rate). In addition, we’ll factor in the 3.8% Medicare tax.

Assuming a combined 40.8% marginal tax rate on investment income, the after-tax yield on the high-yield muni index was 8.9%, based on the Bloomberg Barclays Muni High Yield Index as of January 30, 2018.

Diversification is the other critical reason to consider reallocating from taxable high yield. Municipals, for example, have often exhibited relatively low correlation to equities.

In a sense, higher income municipals occupy a sweet spot in portfolio construction. The asset class offers yield at a level that should satisfy many income seekers, but without the high correlation to equities that has so often seen taxable high-yield selloff alongside equities.

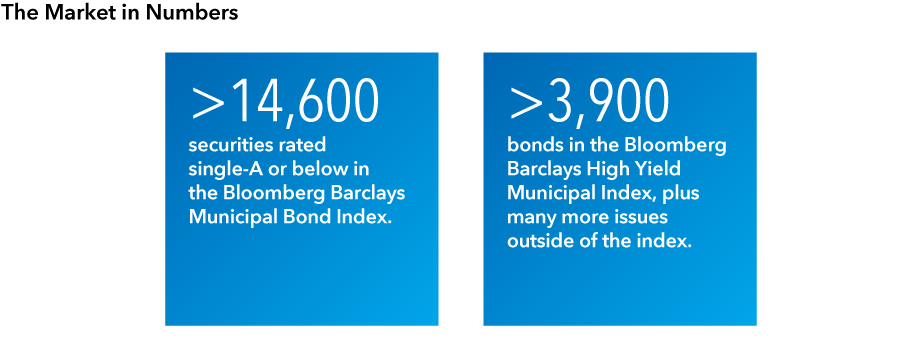

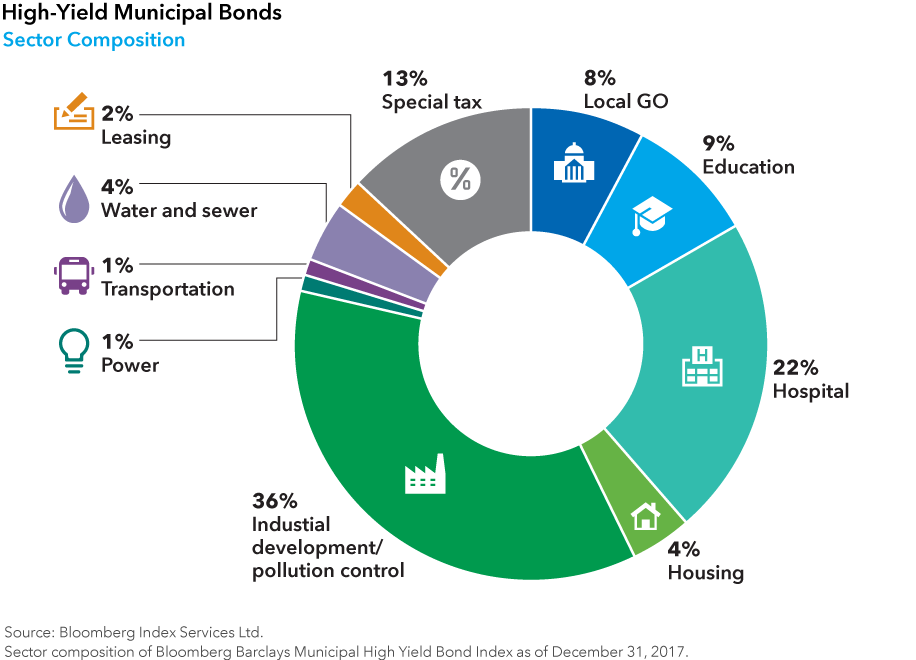

There are diverse opportunities in high-income municipals

State issuers are often top-of-mind for many investors, but it’s important to remember that most municipal issues are revenue bonds.

Unlike general obligation bonds, revenue bonds are backed by a specific revenue stream that is used to service the debt obligation.

In other words, revenue bonds have no direct connection to the pension and other long-term liability issues confronting some state and local governments.

An emphasis on bond-by-bond fundamental research is critical for uncovering compelling risk-adjusted relative value.

In recent years, for example, our high-income strategy — American Funds High-Income Municipal Fund® — has found some diverse prospects.

There have been opportunistic investments around trouble spots like Puerto Rico and Chicago. And there have been many more enduring themes such as consolidation among not-for-profit hospitals. At year-end 2017, about 56% of the fund's portfolio was invested in bonds rated investment grade.

Conclusion

High-yield bonds — no matter where they are from — involve more risk than higher rated, lower yielding bonds. Headline-grabbing financial woes in Puerto Rico and elsewhere have underscored this fact for investors in municipals.

On the other hand, the interest rate risk of municipals is not as widely appreciated. At recent valuations, it’s reasonable to anticipate that a rise in Treasury yields — perhaps in response to interest rate hikes by the Federal Reserve — could be a headwind for near-term municipal bond returns. Already this year we've seen municipal bond returns take a hit as Treasuries sold off.

The silver lining for investors considering a reallocation in 2018 is that volatility may create attractive entry points.

In addition to rising Treasury yields, developments around the Trump administration’s efforts to reform health care and boost infrastructure spending are possible sources of volatility to keep an eye on.

Whatever happens in the market this year, the bottom line for longer term investors is clear: high-income municipal strategies such as American High-Income Municipal Bond Fund offer a tax-advantaged way to upgrade bond portfolios.

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries.

Unlike mutual fund shares, investments in U.S Treasuries are guaranteed by the U.S. government as to the payment of principal and interest. In addition, certificates of deposit (CDs) are FDIC-insured and, if held to maturity, offer a guaranteed return of principal.

The use of derivatives involves a variety of risks, which may be different from, or greater than, the risks associated with investing in traditional cash securities, such as stocks and bonds.

S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.

The market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

© 2018 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Income from municipal bonds may be subject to state or local income taxes and/or the federal alternative minimum tax. Certain other income, as well as capital gain distributions, may be taxable. The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings.

Lower rated bonds are subject to greater fluctuations in value and risk of loss of income and principal than higher rated bonds.

The Bloomberg Barclays U.S. High Yield Index covers the universe of fixed rate, non-investment grade debt.

Bloomberg Barclays U.S. Corporate High Yield 2% Issuer Capped Index covers the universe of fixed-rate, non-investment-grade debt. The index limits the maximum exposure of any one issuer to 2%.

Bloomberg Barclays High Yield Municipal Bond Index is a market-value-weighted index composed of municipal bonds rated below BBB/Baa.

Bloomberg Barclays U.S. Aggregate Index represents the U.S. investment-grade fixed-rate bond market.

Bloomberg Barclays Municipal Bond Index is a market-value-weighted index designed to represent the long-term investment-grade tax-exempt bond market.

Bond ratings, which typically range from AAA/Aaa (highest) to D (lowest), are assigned by credit rating agencies such as Standard & Poor's, Moody's and/or Fitch, as an indication of an issuer's creditworthiness.

Bloomberg® is a trademark of Bloomberg Finance L.P. (collectively with its affiliates, “Bloomberg”). Barclays® is a trademark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Neither Bloomberg nor Barclays approves or endorses this material, guarantees the accuracy or completeness of any information herein and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2018 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

Our latest insights

-

-

Market Volatility

-

Market Volatility

-

Market Volatility

-

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.