Market Volatility

Categories

Market Volatility

Brace for volatility as U.S.-China trade dispute worsens

Jared Franz

Jared Franz

Stephen Green

Stephen Green

Ritchie Tuazon

Ritchie Tuazon

December 10, 2018

With the sharp decline in global equities and U.S. Treasury yields since early October, financial markets appear to be re-pricing the outlook for global growth.

Several signals indicate investors are looking past the current strength in the U.S. to the potentially damaging impact of escalating U.S.-China tensions on the global economy. These include an inversion of the Treasury yield curve from two-year to five-year maturities. Futures markets are also reining in expectations of rate increases by the Federal Reserve in 2019, and even pricing a higher probability of a rate cut rather than further rate hikes in 2020.

That both the U.S. and China — the world’s two largest economies — are in the late stages of the economic cycle with limited resources to spur growth is further weighing on investor sentiment. On top of that, European growth has disappointed as the highly trade-dependent economy has suffered the most from global trade disruptions.

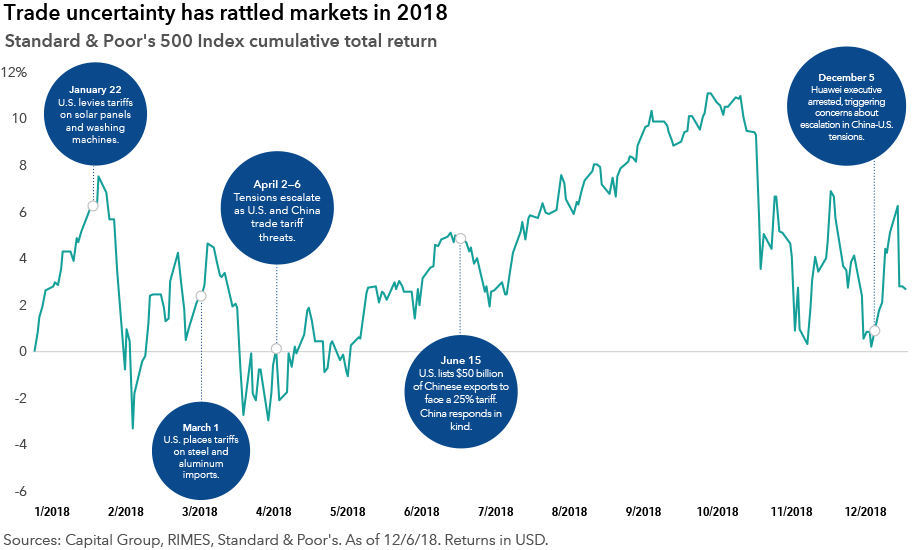

It is then no surprise that market sentiment has followed the direction of China-U.S. negotiations on trade and other economic matters — with the arrest of a senior executive at China’s telecom giant Huawei presenting an unexpected turn of events. As the U.S., China and Europe seek to rewrite the rules of world commerce in their favor, investors will need to brace for heightened market volatility in the year ahead.

To get clarity and perspective on these market dynamics and the factors driving them, we provide the following insights from three of Capital Group's investment professionals.

China-U.S. relations will continue to drive market sentiment.

As we monitor the ongoing negotiations between the U.S. and China on trade, tariffs, intellectual property protection and a host of other issues, we need to acknowledge that the relationship has fundamentally changed and evolved into one that is increasingly competitive and tense. Moreover, the two sides are still too far apart, and neither has suffered sufficient economic pain to make any real compromises.

The arrest in Canada of Meng Wanzhou, Huawei CFO and vice chair, and daughter of founder Ren Zhengfei on December 1 was the latest blow in an increasingly tense relationship between the countries. The arrest has significant ramifications given Huawei’s position as China’s leading hardware firm, biggest patent filer, 4G/5G equipment giant, leading chip designer, smartphone champion and most globalized company (with about 30% of revenues coming from overseas).

Clearly, some kind of talks leading to a ceasefire on further tariffs would lift market sentiment — and given the scale of what’s threatened, would have a substantive impact on the outlook for the U.S. and Chinese economies. On the other hand, a stalemate in negotiations after expectations were raised at the G-20 summit in Argentina will continue to disappoint market participants.

Moves in the making

As companies around the world look to the future, many are already making plans. Final-assembly electronics firms are establishing and expanding facilities outside of China at the demand of their U.S. clients. Thailand seems popular for electronics firms and Vietnam already dominates in apparel and textiles. U.S. tariffs have accelerated decision-making that was already under consideration by many companies due to rising costs in China. Firms are generally not shutting down their China facilities, at least for now, though attrition might mean their overall employment will fall.

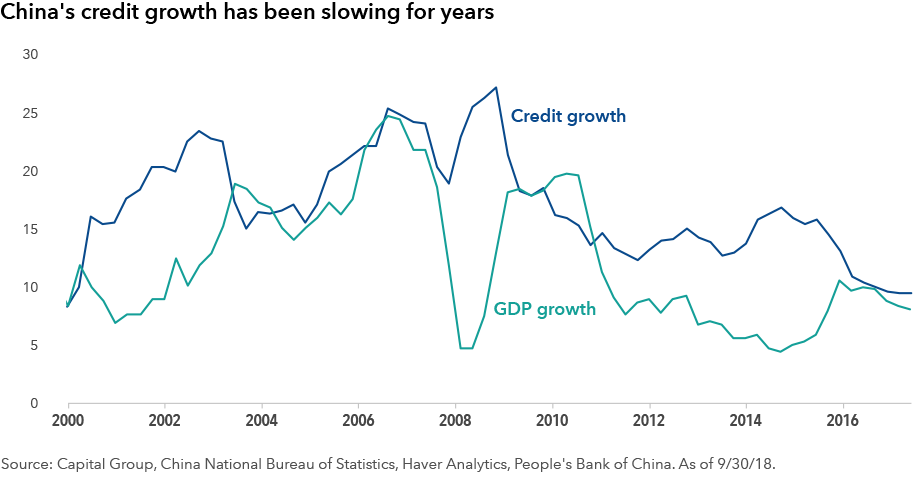

On the domestic front, China is coping with a deceleration in economic growth. There are signs of weakness emerging in the labor market. While middle-class, white-collar income gains remain strong, unskilled wages are rising slowly. Consumer confidence is off its highs, but still good. Consumer credit growth is declining, however, leading to sluggish car sales and lower revenues in Macau, which tend to be early indicators of softening demand.

Business confidence has weakened and with the threat of additional tariffs, I do not see it returning anytime soon. So I think several of China’s economic measures will continue to deteriorate. China’s authorities will likely provide fresh fiscal and monetary stimulus as the slowdown becomes more painful, with the March–April 2019 period following the Chinese New Year likely to see a bigger pro-stimulus push.

Negotiations between the U.S. and China are likely to move in fits and starts. In addition to trade, sensitive technologies will continue to be areas of contention. Both countries are facing challenges in their economies and each side has many incentives to strike compromises. But both the U.S. and China also have distinct strategic, long-term objectives that are at odds with each other. Against this backdrop, investors should be prepared for a period of elevated market volatility.

Decoding the yield curve’s message

The U.S. Treasury yield curve from the two-year to the five-year maturity points has inverted, meaning that five-year bond yields dipped below two-year yields. It is the first time this has happened since 2007. Why did it happen and what does it mean?

Historically, an inverted yield curve has been a telltale sign that the bond market is pricing in a tough economic environment ahead. It's created when the Federal Reserve tightens monetary conditions via its more direct control of short-term interest rates. Long-term rates, largely controlled by market forces, drift lower when investors start to believe the Fed's tightening will lead to economic contraction, lower rates, lower inflation and eventually fresh rate cuts. A positive sloping yield curve, on the other hand, is a signal the bond market is looking for a mix of strong growth and inflation.

The primary driver of this yield curve inversion was a tightening in financial conditions and a Federal Reserve that has grown more dovish. In the months of October and November, a stronger dollar, wider credit spreads and weak equity markets all contributed to tighter financial conditions. The Federal Reserve looks at financial conditions as a real-time monitor for future economic conditions and has taken note of this inversion.

In recent speeches, Federal Reserve Chairman Jerome Powell and Fed Governor Lael Brainard appear to have taken note of market moves, shifting their rhetoric to be more dovish. Bond markets took note, bringing down expectations of rate increases in 2019 from over two hikes to less than one hike. Furthermore, markets have shifted rate expectations in 2020 and 2021 from a Fed that is more likely to raise rates to a Fed that is more likely to cut — a tacit acknowledgement that a slowdown is coming.

I think the market view is reasonable. The probability of cuts in 2020 and 2021 should indeed be higher than hikes. With the effects of fiscal stimulus wearing off in 2019, and growth in China and Europe softening, it might be difficult for the U.S. to continue to anchor the global economy. Recent business investment has not been robust, which further dampens future growth prospects.

A few things to keep in mind about an inverted yield curve:

- Of the eight instances when the two-year to five-year portion of the curve has inverted going back to 1972, six of those instances saw a recession within two years, and all eight saw the Fed cut rates within two years.

- Not everyone seems to pay attention to the same part of the curve: The two- to five-year part of the curve gets less attention. Bond investors and academics tend to pay more attention to the two- to 10-year part of the yield curve, which has not inverted yet, but which could happen if financial conditions remain tight.

- When looking at two- to 10-year maturities, an inverted yield curve has preceded every recession since 1950. That said, there have been two times that the curve inverted and no recession followed.

- The exact timing of the recession following an inverted yield curve has varied from nine months to over two years. It is a warning signal glowing orange, but not bright red.

Despite late cycle, a U.S. recession is not a foregone conclusion.

The U.S. continues to exhibit late-cycle characteristics. The labor market is tight with rising wages and cost pressures. The Fed has responded by raising interest rates in line with what they have signaled through the “dot plot” and reduced liquidity via reduction in its balance sheets. Quantitative tightening and a strong dollar trend are also causing global central bank liquidity to decline faster than expected and resulting in higher funding costs for U.S. borrowers.

In addition, non-U.S. growth is a bit softer than expected. Leading indicators of activity in China and Europe continue to slow while Chinese stimulus is not expected to provide an offset until late in 2019. Macro and financial imbalances continue to build. Corporate and government debt is on a steady rise. The fiscal stimulus has created deficits of an estimated 5.0% to 5.5% of GDP in 2018, a peak in the period since the financial crisis of 2008.

Recession coming in 2020?

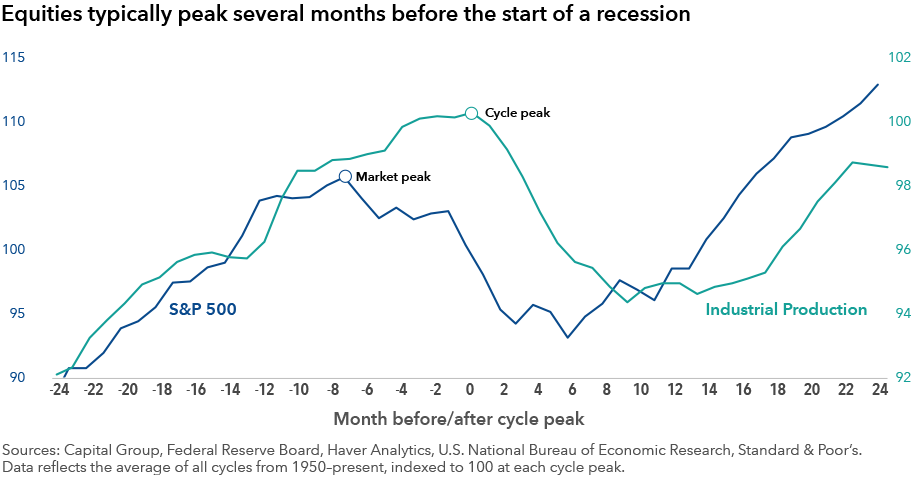

As fiscal spending increases, deficits should widen. Shadow banking is growing, and companies continue to take on debt to make dividend payments, implement share buybacks and fund M&A activity. The economic cycle appears to be evolving on a path that suggests weakness sometime in 2020, although this may not translate into a full-blown recession. Moreover, stock markets peak on average six months prior to the economic cycle. But we don’t think a recession is starting in the near-term, so we could see a bounce back in equities at some point before then.

In my view, the probability of an entrenched equity bear market in the next six months remains low. The Fed has indicated it will be responsive to economic data, the widening in triple-B corporate bond spreads has been moderate, equities have modestly re-rated and there will be the lagging effect of fiscal stimulus. Corporate earnings growth will decelerate but should remain in the mid-single digits.

The major risk to this view will be the trajectory of U.S.-China trade negotiations, as a further escalation could create a negative feedback loop. This is a very fluid situation that we will monitor closely.

In periods of heightened market volatility, investors can benefit by:

- Maintaining a broadly-diversified portfolio

- Having a portion of their portfolio in liquid assets, such as cash and high-quality bonds

- Making certain that a portion of their fixed income allocation provides diversification from equities

- Holding a combination of growth and dividend-oriented strategies in their equity allocation

Learn more about

The Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks. This index is unmanaged, and its results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes.

Our latest insights

-

-

Market Volatility

-

Market Volatility

-

-

Artificial Intelligence

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.