Market Volatility

Categories

Fixed Income

The outlook for credit in a recessionary economy

Damien McCann

Damien McCann

May 20, 2020

KEY TAKEAWAYS

- Despite support from the Federal Reserve, downgrades are poised to be more prevalent than in previous cycles

- The full financial impact of COVID-19 on corporate America will become clearer over the next few quarters

- For investors who can take a long-term view and be selective, current high-yield valuations are attractive

With the severity and duration of the economic downturn still unclear, investors may be wondering what this means for corporate credit, particularly the riskier high-yield sector.

We talked with Damien McCann, lead portfolio manager for American Funds Multi-Sector Income FundSM to get his perspective on the broader credit market and how companies are traversing the pandemic.

What’s your outlook from here?

We’re in a period of incredible uncertainty given the unknown path of the virus. We do know, however, that much of the economy has been significantly disrupted by the pandemic. Revenues and cash flows in many industries are currently under severe pressure. Other industries are faring much better. Second quarter earnings will be ugly but should represent the bottom for most companies. More important than second quarter earnings, however, will be what managements of companies are seeing for third and fourth quarter activity.

My base case is that the economy is beginning to improve as we speak, and that this recovery will continue through the remainder of the year and 2021. How fast is unknown. I expect an uneven recovery by industry and more volatility given the unprecedented economic disruption and the many uncertainties regarding the spread of the virus, containment efforts, and progress on therapies and vaccines.

Is this downturn different from the global financial crisis (GFC)?

Each is similar and different. Similarities with the GFC include the significant economic contraction and related sharp rise in unemployment. Both periods include significant stock and bond market volatility, as well as a seizing up of credit markets. Both periods have received significant stimulus and support by governments and central banks.

But the drivers of each downturn are very different. The GFC came from within our economy and markets. The pandemic is an exogenous shock, and the hit to economies is more severe than during the GFC. The monetary and fiscal stimulus came much faster this time around, and in much larger size, because policymakers have learned from the past and want to prevent a severe recession from becoming a financial crisis.

The Fed is actively supporting numerous markets — including U.S. Treasuries, mortgages and credit markets. Some of this, such as buying corporate bonds and ETFs, is without precedent in the U.S. In my view, these programs indicate a deep commitment by the Fed to ensure credit markets continue to function. This helps explain why credit markets have responded favorably and, after widening dramatically in mid-March to the widest levels on record for a few days, spreads recovered some of that widening later in the month.

What steps are companies taking to manage through this period?

Companies are grappling with a high level of uncertainty about the duration of the downturn. As a result, many companies are taking steps to bolster liquidity. In other words, companies are trying to build up a lot of cash so they can survive this period. Steps companies are taking to build cash include cutting operating expenses and capital outlays, reducing or eliminating dividends and share repurchases, and raising capital.

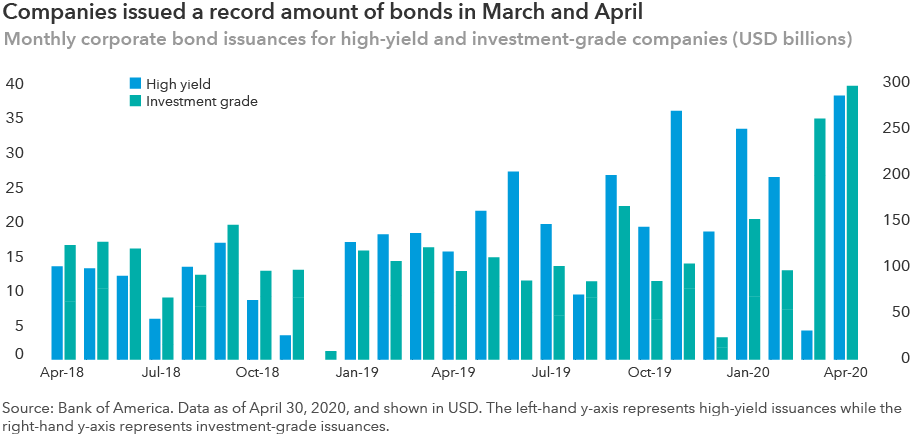

On this last point, the Fed’s injection of liquidity and its direct participation in corporate bond markets have restored order to markets and made it possible for investment-grade companies and certain high-yield issuers to borrow again.

The combination of the Fed’s support for credit markets, and the severity and uncertainty of the downturn, has led to record levels of investment-grade bond issuance in recent months. Certain companies, such as Disney, have tapped the bond market more than once recently. What’s more, companies in the eye of the storm — including certain leisure and travel-related issuers — have been able to access markets.

What is your expectation for default rates?

I expect defaults and downgrades to be higher than in prior cycles given the severity of the economic contraction. In fact, U.S. corporate downgrades have spiked to their highest level in more than a decade in the first quarter, according to data from Standard & Poor’s.

Companies that are more exposed to economic disruption, as well as those with more leverage and less liquidity, are most vulnerable to defaulting. Despite efforts to cut costs and preserve cash, some companies won’t be able to handle the sudden near full stoppage of economic activity.

I expect downgrades to exceed previous cycles, with the potential for bankruptcies of companies in the U.S. high yield and loan market to exceed 10% over the next year.

Can you provide some color on “fallen angels” — the large companies such as Ford that have recently entered the high-yield market? How does that impact the high-yield market?

Credit rating agencies have been more aggressive with downgrades in recent years. Given the magnitude of the economic contraction I expect this to continue. There will certainly be many downgrades in the months and quarters ahead.

I also expect more companies to enter the high-yield sector. Some investors fear that a rash of supply in this sector could overwhelm the market, but keep in mind that it has actually shrunk in recent years on fewer issuances and more companies turning to the loan market. In that sense, the high-yield market could use some additional supply. Also, the Fed’s move to scoop up corporate debt should help absorb the shock. In some cases, these downgraded bonds could represent attractive investment opportunities in high-yield portfolios.

In what areas are you finding value?

As I look across the corporate market, exposure to this pandemic and economic contraction varies dramatically by industry and company. For example, at one extreme are certain insurance underwriters that have become more profitable due to fewer claims in this environment. At the opposite extreme are certain leisure companies that have seen revenues fall to zero. But even within this sector, exposure varies significantly based on the business model and balance sheet. Some leisure companies adapt and survive better than others.

The variation in exposure to the pandemic represents an incredible opportunity for deep, fundamental credit research to add value in portfolios. Our credit analysts are well versed on their companies and are in regular contact with managements. They are identifying and investing in issuers they believe have the ability to navigate this period.

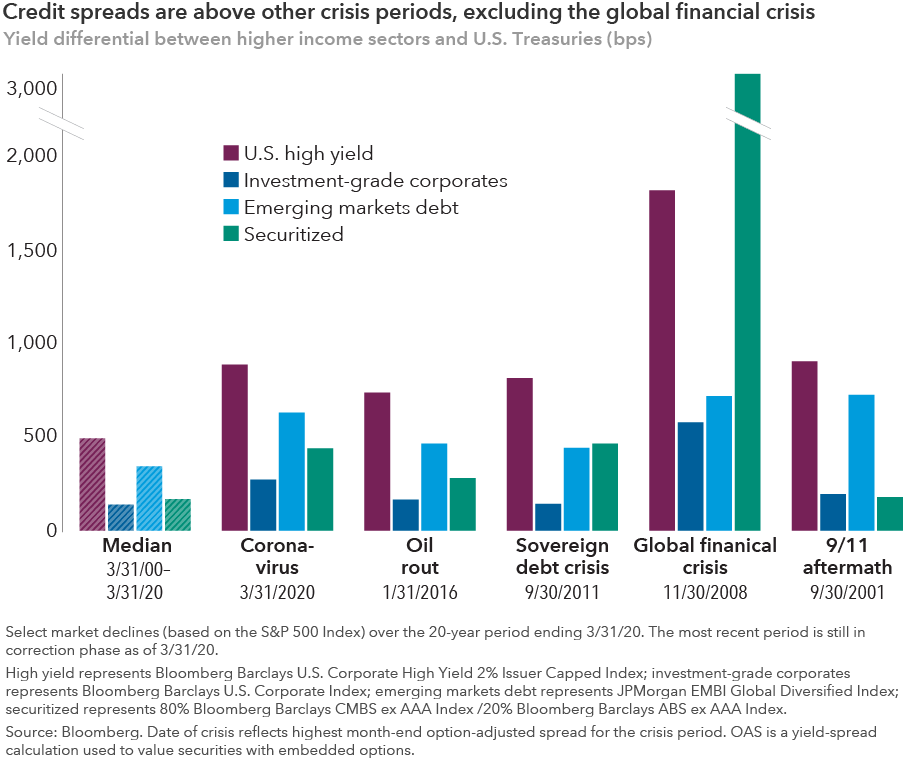

Market events like this can and have historically represented a good entry point for long-term investors. Spreads today are broadly comparable to past crises and recessions, excluding the global financial crisis. I don’t believe in timing the market but do feel that current spreads provide an opportune entry point for a long-term investment strategy.

What about relative value between investment-grade and high-yield bonds? And what about the BBB-rated area of the market?

While income opportunities are higher in both investment-grade and high-yield corporates, I’ve been finding even more in high yield. In particular, the improved valuations have led to more opportunities within health care, technology companies and consumer staples.

The BBB market is huge (nearly $3T) and very diverse. The work our analysts have done suggests that a large majority of this particular market is unlikely to fall to high yield during this period. Many BBB companies are considered high quality and resilient. Some of the BBBs that fall to high yield will be attractive investment opportunities within that space, particularly if the downgrade leads to wider credit spreads.

How is Capital navigating this environment?

From a credit perspective, we are diving deep into understanding which companies will come out of this crisis intact and be able to repay their lenders. Our strong relationship with management teams and focus on fundamental credit research help us in this endeavor, as it’s our belief that that the prospects for recovery will very much be company, industry and geographically specific.

We remain very selective about our investment decisions, which are made on a security-by-security basis. This is especially important in today’s environment as downgrades and defaults become more frequent. Knowing what you’re buying helps mitigate broader credit market risks.

We also can’t stress enough the benefits of a long-term perspective, as a multiyear view may provide investors with the opportunity to capture higher returns.

Learn more about

Bond ratings, which typically range from AAA/Aaa (highest) to D (lowest), are assigned by credit rating agencies such as Standard & Poor's, Moody's and/or Fitch, as an indication of an issuer's creditworthiness. If agency ratings differ, the security will be considered to have received the lowest of those ratings, consistent with the fund's investment policies. Securities in the Unrated category have not been rated by a rating agency; however, the investment adviser performs its own credit analysis and assigns comparable ratings that are used for compliance with fund investment policies. The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings. Investments in mortgage-related securities involve additional risks, such as prepayment risk, as more fully described in the prospectus. Higher yielding, higher risk bonds can fluctuate in price more than investment-grade bonds, so investors should maintain a long-term perspective.

Bloomberg Barclays U.S. Corporate Investment Grade Index represents the universe of investment grade, publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity and quality requirements. Bloomberg Barclays U.S. Corporate High Yield 2% Issuer Capped Index covers the universe of fixed-rate, non-investment-grade debt. The index limits the maximum exposure of any one issuer to 2%. The 80%/20% Bloomberg Barclays CMBS ex AAA Index/Bloomberg Barclays ABS ex AAA Index blends the Bloomberg Barclays CMBS ex AAA Index with the Bloomberg Barclays ABS ex AAA Index by weighting their cumulative returns at 80% and 20%, respectively. The Bloomberg Barclays CMBS ex AAA Index tracks investment-grade (Baa3/BBB- or higher, excluding Aaa/AAA) commercial mortgage-backed securities that are included in the Bloomberg Barclays U.S. Aggregate Index. The Bloomberg Barclays ABS ex AAA Index covers fixed-rated investment-grade (Baa3/BBB- or higher, excluding Aaa/AAA) asset-backed securities that are included in the Bloomberg Barclays U.S. Aggregate Index. The index has three subsectors, which includes credit and charge cards, autos and utility. Bloomberg® is a trademark of Bloomberg Finance L.P. (collectively with its affiliates, “Bloomberg”). Barclays® is a trademark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Neither Bloomberg nor Barclays approves or endorses this material, guarantees the accuracy or completeness of any information herein and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The J.P. Morgan Emerging Market Bond Index (EMBI) Global Diversified is a uniquely weighted emerging market debt benchmark that tracks total returns for U.S. dollar-denominated bonds issued by emerging market sovereign and quasi-sovereign entities. This report, and any product, index or fund referred to herein, is not sponsored, endorsed or promoted in any way by J.P. Morgan or any of its affiliates who provide no warranties whatsoever, express or implied, and shall have no liability to any prospective investor, in connection with this report. J.P. Morgan disclaimer: https://www.jpmm.com/research/disclosures.

Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks. Standard & Poor’s 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2020 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC. Investors cannot invest directly in an index.

Our latest insights

-

-

Market Volatility

-

Market Volatility

-

Market Volatility

-

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.