Walking the showroom floor of Germany's international auto show used to be a time to admire the latest and greatest gas-powered Mercedes-Benz, Volkswagen or even a Bentley. Not so much this year. One can sense the electric vehicle future coming. Two questions are at the forefront of people's minds: Will European consumers be interested in buying Chinese electric vehicles (EVs), and will China’s automakers slash prices to grab market share?

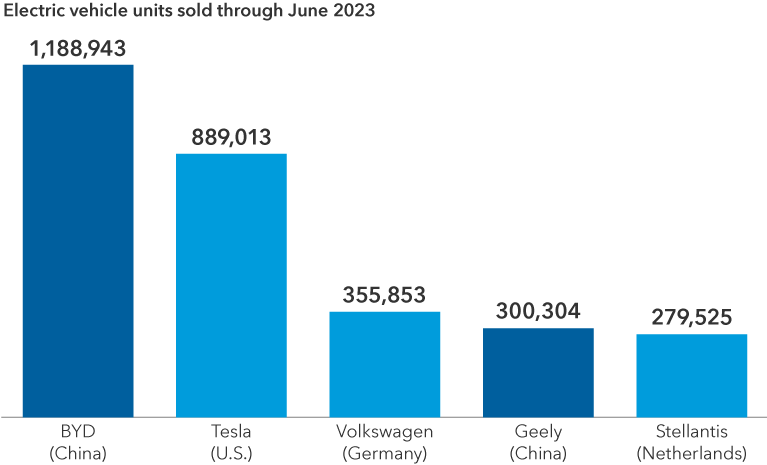

China has surpassed Japan as the top global automobile exporter so far this year, a feat that was unimaginable a decade ago. Several of China's leading EV makers are starting to charge into Europe's market, marking an early litmus test of demand in developed markets for Chinese EVs.

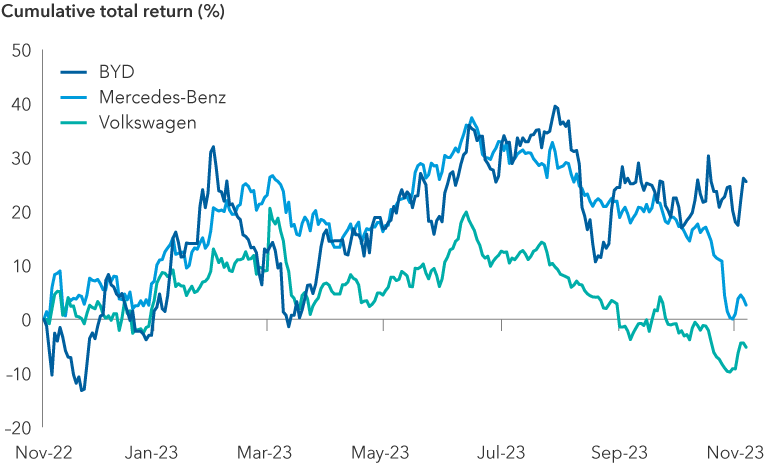

It's already having ripple effects in Europe, where regulators and politicians are grappling with how best to protect their traditionally strong auto industry. It's too early to know how the situation plays out, but it seems clear it will change the operating dynamic for Europe's automakers and how investors value their businesses moving forward.

Based on conversations with industry officials and company executives during our recent trip to Munich, here are several implications we are watching closely.