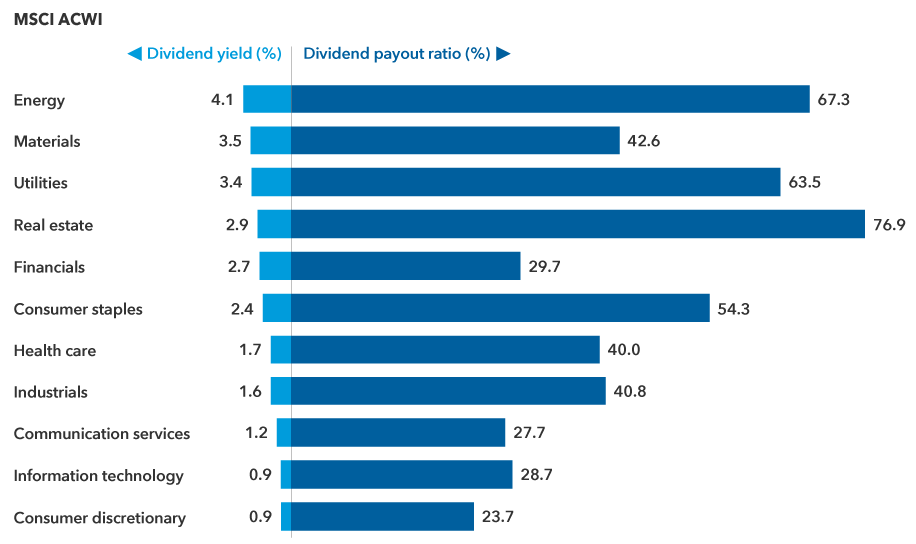

4. Financials, energy and health care are areas of dividend opportunity

Financials, energy and health care represent a substantial chunk of the dividend-paying universe, and a confluence of factors appear to support the case of rising dividends from each of these areas.

Financials: Rising rates should help the more rate-sensitive banks in the U.S. and Europe expand their net interest margins, which have been suppressed for many years by persistently low interest rates. This could result in stronger earnings, improved dividend streams and higher valuation multiples.

Banks have been building up excess capital on their balance sheets since the Great Financial Crisis and most are now well-capitalized, having undergone a number of regulatory stress tests. And some banks in the U.S. and Europe are poised to redeploy surplus capital in the form of regular and catch-up dividends after facing regulatory limitations during the pandemic.

For example, Dutch banking giant ING has committed to a minimum 50% dividend payout ratio (the proportion of earnings paid out as dividends to shareholders, typically expressed as a percentage) of earnings. CaixaBank, one of Spain’s largest banks, stated it would boost its payout ratio to as much as 60% from 50% previously. It’s possible that other European banks could follow a similar course of action as regulatory pressures ease, making this sector a potential source of more consistent dividend income.

Energy: Large integrated oil companies have long been good sources of consistent dividends for income-oriented investors. They’ve also become more disciplined on supply, having curtailed investment in existing reserves and pursuing new sources of oil.

U.S. oil giants Chevron and Exxon Mobil have demonstrated a steadfast commitment to paying dividends despite some dramatic swings in the price of oil over the past decade. Chevron recently increased its dividend for a 35th consecutive year.

But dividend policies have diverged in the oil sector and calibrating the dividend streams of oil companies has become more challenging. Over the past couple of years, European oil majors BP and Royal Dutch Shell have cut their dividends amid their transition to investing in renewable energies that are capital intensive and where the return on invested capital is still uncertain. Having reset their dividends to lower payout ratios, the European oil majors have left sufficient room to increase dividends over time.

Health care: Health care companies could be a source of both earnings and dividend growth in the current inflationary environment. Pharmaceutical companies historically have exhibited relatively strong pricing power. While the industry has faced political pressures on drug prices, the more innovative pharmaceutical companies will likely be positioned to raise prices at modest levels.

Like the energy companies, the major pharmaceutical companies recognize that a sizeable portion of their value proposition with the investor base is the dividend payout. That, combined with the potentially robust pipeline over the next several years at several major pharmaceutical companies across all geographies, gives us confidence that this will be another area that can be a well-diversified source of equity income.