Yield Curve

Anmol Sinha

Anmol Sinha

After much anticipation, the U.S. Federal Reserve kicked off its monetary easing cycle in September with a 50-basis-point reduction of the federal funds rate. Treasury yields rallied ahead of the meeting, ending the prolonged inversion of the yield curve: 10-year yields moved above 2-year yields for the first time since July 2022.

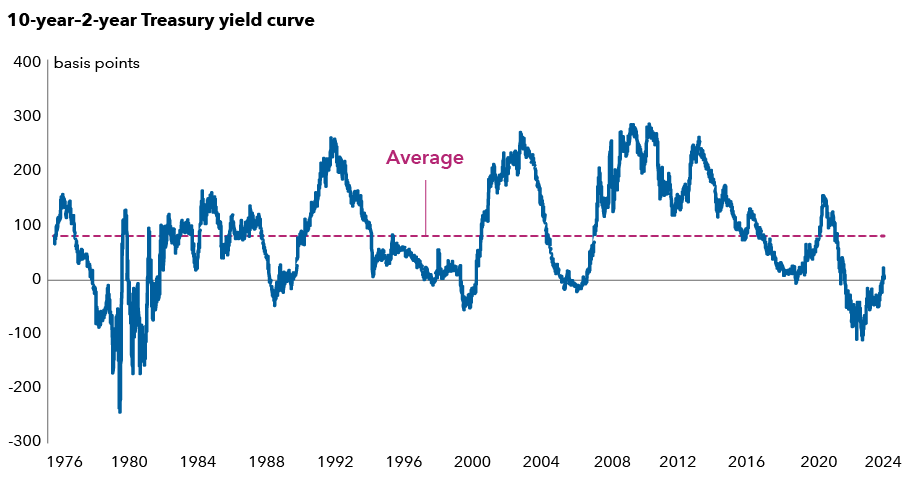

Yield curve remains well below historical average level

Source: Federal Reserve Bank of St. Louis. Data as of October 10, 2024. The 2s10s Treasury curve represents the 10-year Treasury yield spread over the 2-year Treasury yield.

Capital Group’s interest rates team has a long-held conviction in a yield curve steepener. This can happen either by short-term yields falling more than long-term yields and/or long-term yields rising more. This should normalize the curve to be upward sloping. Now that the Fed has delivered its first policy rate cut, the team expects the curve could steepen more meaningfully.

The chart above shows the difference between the 10-year yield and 2-year yield remains notably smaller than its 50-year average. In the post-Volcker era (Paul Volcker served as Fed chair from 1979 to 1987), when the curve previously inverted, it has tended to steepen significantly after moving back into positive territory. The interest rate team now favours greater emphasis on steepening in this portion of the curve.

They also expect yield curve positioning to complement attractive opportunities in sectors, such as corporate and securitized markets. A steepening bias should help hedge several potential adverse economic scenarios for risk assets.

The Fed’s messaging suggests it believes current policy is restrictive, and the U.S. rate reduction cycle is just beginning. A significant decline in inflation, from over 9% in mid-2022 to 2.5% in August, has given the Fed additional capacity to ease policy rates. Valuations also indicate further curve steepening potential beyond what is priced in by markets.

A more pronounced slowdown in economic growth or deterioration in the labour market could drive the front-end of the yield curve lower. Meanwhile, the resilience of the U.S. economy makes a hard landing or recession scenario less likely, but the risk may be underestimated by markets. Weakness in the economy or a sustained rise in unemployment could trigger a larger than expected Fed response, leading to a greater steepening of the curve.

Additionally, concerns about the high U.S. fiscal deficit and higher supply of Treasuries could resurface and put upward pressure on long-end yields, especially as investors demand higher term premiums. With the deficit at high levels for a non-recessionary environment, there’s potential for further steepening, even with resilient economic growth.

The Volcker Shock — A period of historically high interest rates, ignited by Federal Reserve Chair Paul Volcker's choice to raise the central bank's key interest rate to curb inflation. Volcker served as Fed chair from 1979 to 1987.

A yield curve illustrates the yields on similar bonds across various maturities. An inverted yield curve occurs when yields on short-term bonds are higher than yields on long-term bonds. Yield curve steepening occurs when long-term rates rise more than short-term rates, or short-term rates fall more than long-term rates.

Our latest insights

Commissions, trailing commissions, management fees and expenses all may be associated with investments in investment funds. Please read the prospectus before investing. Investment funds are not guaranteed or covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. For investment funds other than money market funds, their values change frequently. For money market funds, there can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian investment funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2025 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2025. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.