Do proposed stimulus measures in China change the trajectory of its equity market and the economy? It will take more time to see what transpires, but recent actions are steps in the right direction, and as longtime China watchers, we are encouraged by the developments.

Following a slew of announced policy measures, including interest rate cuts, reductions in existing mortgage rates and billions in funds for state-owned firms to buy domestic equities, we think the intent of party leaders is now clearer.

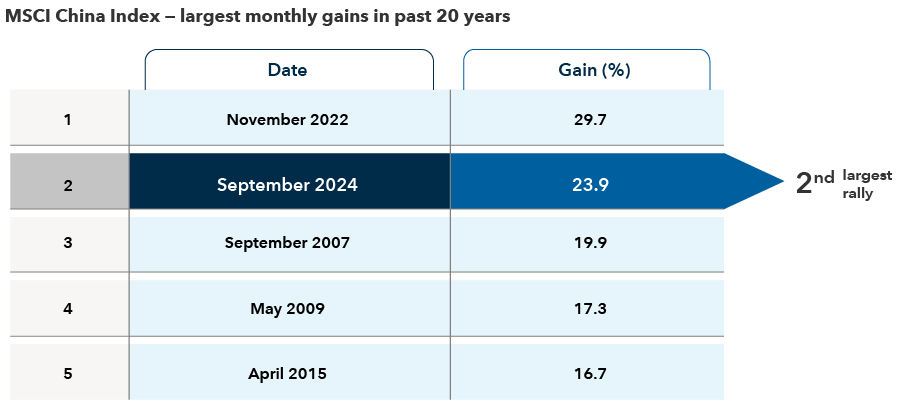

Top policymakers have acknowledged they must stop the decline in home prices to shore up the economy and consumer confidence. This is a significant development and a change in stance from four years ago. The impact has been felt in the stock market, with the MSCI China Index rallying 16% the last week of September, although the pace of gains has since slowed.