Too busy to plan your next business trip? Imagine this scenario: You set a date and destination in your digital calendar and then a bot powered by artificial intelligence (AI) does the rest. It searches for the cheapest flight that complies with your employer's work travel policies, picks your preferred aisle or window seat, pays for the ticket, and adds it to your calendar.

Science fiction? This reality may not be too far in the future.

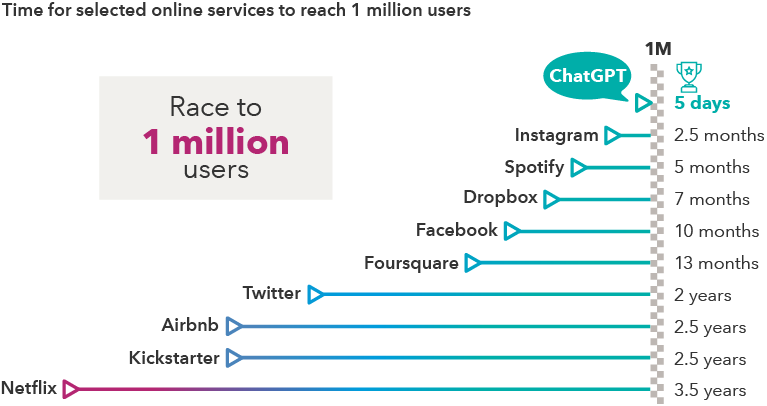

Given the vast potential of AI, it's no surprise the market has sought to sniff out early winners and losers. Many technology stocks have soared since ChatGPT captured the public's imagination earlier this year.

We believe this is the start of the next megacycle for the technology sector. But it won’t be linear, and investors will need to be nimble. Stock prices will likely go through fits and starts, with stocks getting overextended at times and pulling back when the market doubts progress.

There are also outstanding questions about AI's impact on society and how best to regulate its development. With that in mind, here are six unfolding themes we are tracking that have potential impacts on companies and markets.

.png)