Marketing & Client Acquisition

6 MIN ARTICLE

For advisor use only. Not for use with investors.

While estimates of the great wealth transfer from the baby boomer generation vary widely — anywhere from $30 trillion to $68 trillion at last count — the fact remains that generations of inheritors will be looking for professional financial guidance in the coming decades.

But it’s not just investment expertise that will win the business stemming from this money in motion, says Leslie Geller, wealth strategist at Capital Group. “One aspect that’s often overlooked is that large inheritances don’t come in the form of lump sums that are ready to invest. Instead, they will very often be in the form of trusts, which will come with a lot of legal and technical issues,” she says. Having the ability to help with those issues, and to get the family involved in planning for them, is one way advisors can add value.

With all that potential business out there, how do you reach and engage these multigenerational clients? Here are a few ideas to consider.

Get to know clients’ families

If you have a family-focused practice, you may be familiar with clients’ children and grandchildren. You may have even engaged them with regular birthday and graduation cards. But getting to know them as adults may take a bit more work on your part.

One way to start making those family connections is through social media. If your knee-jerk reaction is that your high net worth clients aren’t on social media, you may be missing the bigger picture. While your clients may not be on social media, their kids and grandkids may well be. There are more high net worth individuals on LinkedIn than you might think, and that platform offers a perfect opportunity to reach out and introduce yourself to family members.

Another important step for next-generation planning involves getting serious about tech. This means not only being able to talk to them on social media, but also having a strong digital presence in general. Younger investors are used to comparing brands and validating decisions online, and are more likely to do business in a virtual arena. The good news is that a strong digital strategy can be a major differentiator in driving business growth. Only 14% of advisors in our Pathways to Growth: 2024 Advisor Benchmark Study considered themselves expert in marketing or digital marketing. But among the highest growth practices, that number grew to 24%.

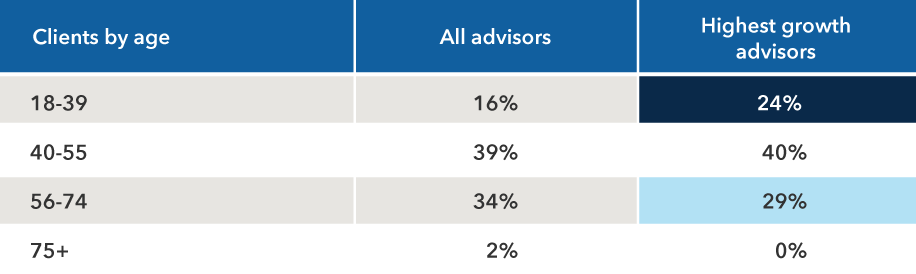

The truth about youth

In our recent advisor benchmark study, the highest growth segment was more likely than the average advisor to serve clients under age 40.

Source: Capital Group, Pathways to Growth: 2023 Advisor Benchmark Study

Offer next-generation planning

It’s always tempting to dismiss the younger generation and their unfamiliar ways, but the reality is that younger clients represent the future of your business. You can invest in this future by finding a way to offer them financial planning services.

Often, how to do this is a matter of staffing. Experienced principal advisors may see value in having junior associates on the team who have the bandwidth and the background to more easily engage with younger generations. Indeed, one industry report recommends that the junior advisor on every team could be commissioned to connect with the next generation of affluent clients.

That’s the strategy taken by advisor Karen DeRose of DeRose Financial Planning Group in Chicago. DeRose hired her two grown sons — one as a paraplanner, the other in marketing — to help her practice better relate to the younger family members of existing clients. A second-generation advisor herself, DeRose’s firm serves at least three generations of clients: those who started working with her father and are now in their 80s and 90s, their children in their 50s and 60s, and grandchildren in their 30s and 40s. Her firm now offers what she calls a “next-gen foundational plan” to help younger clients with buying a home, paying for school, understanding stock options and company benefits, and managing basic financial planning. Longstanding clients love it, she says, because it shows that her team cares about the thing clients value most: their families.

While the work may be foundational, client service expectations remain high. The millennial generation may not have the same assets as their parents or grandparents, but they expect more control over their finances, and they’ll have little problem replacing you with another advisor if you’re not fitting the bill. Geller notes you should consider having younger clients work with someone in a similar demographic — not just on your staff, but in your centre-of-influence network as well. Make sure your list of referrals for tax or estate planning attorneys also includes gender and cultural diversity, says Geller.

Consider a family wealth briefing

Another way to engage multiple generations is by broadening your menu of services to include estate planning and charitable guidance. And get the family involved.

The connection between these value-added services to multigenerational business is clear, says Geller. “If you’re just talking to clients about investments, you’re not getting to families,” she says. “But if you talk to them about tax or estate planning, for example, you’re in a better position to have conversations about longevity, inheritance and implications for the next generation.”

She notes, however, that there’s no reason to feel intimidated by adding these new services. Little things can make a big difference. That is, your tax and estate planning offerings don’t need to be full-scale services in the traditional sense. They can be as simple as facilitating intra-family communication and transparency.

One way to accomplish this, she says, is by holding a family wealth briefing: a virtual or in-person gathering to discuss the ongoing management and governance of the family’s wealth. As a facilitator of this event, the advisor should prepare a careful agenda, which could include:

- Financial education and responsible wealth management

- Family mission and values

- A wealth update or “state of the family” presentation

- Ongoing roles, responsibilities and expectations of family members

Because family dynamics can be challenging even in good times, your goal is to advocate for your client without taking sides. But the more you engage with family members now, the greater the opportunity to work with them after a wealth transfer.

Related content

-

Marketing & Client Acquisition

-