ETF

The biggest trends for active ETFs in 2023

The higher rate environment has resulted in more attractive yields across fixed income, making it a compelling area to consider. Bonds are offering significantly higher yields without having to take on more risk, which means you don’t have to venture too far on the risk spectrum to pursue higher income in a portfolio. Whether you’re tax-loss harvesting and wondering where to reinvest assets or unsure how to navigate fixed income allocations amid unpredictable Fed policy, we’ve identified three reasons why bonds (and active fixed income ETFs) appear compelling in the current environment.

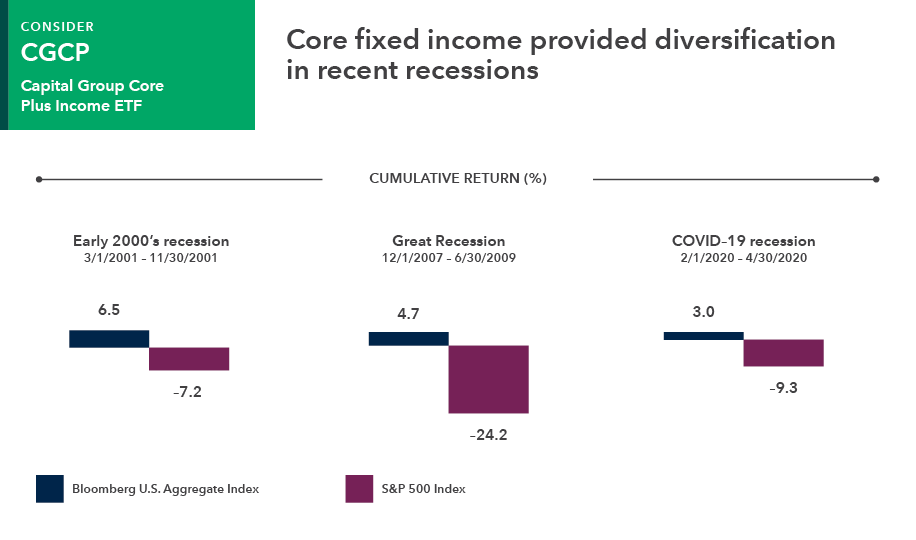

Bonds are expected to return to providing diversification from equities, which will likely be beneficial if there’s a recession.

Sources: Morningstar, Bloomberg Index Services Ltd. Recession periods defined by the National Bureau of Economic Research. Correlations calculated using daily returns. Returns shown are cumulative. Past results are not predictive of results in future periods.

If you’re still holding fixed income funds purchased in early 2022 or before, there may be an opportunity to generate losses to offset gains elsewhere, if any, and lower tax liabilities. However, fixed income tax-loss harvesting opportunities may become scarcer if bond markets continue to recover and inflation pressures recede.

"When it comes to tax-loss harvesting, our active fixed income ETFs can be a compelling investment during the wash sale period† as a way for investors to preserve their allocations and maintain exposure to a changing market while still booking losses."

Holly Framsted

Capital Group Director of ETFs

Source: Morningstar Direct, all data as of 12/31/22. Yield to worst is the lowest yield that can be realized by either calling or putting on one of the available call/put dates, or holding a bond to maturity.

§Tax-equivalent yield as of 12/31/22. The taxable equivalent yield assumptions are based on a federal marginal tax rate of 37%, the top 2022 rate. In addition, we have applied the 3.8% Medicare rate.

The global economy appears to be in the late stages of a market cycle, possibly offering an opportune time to invest in fixed income securities — if you know where to look.

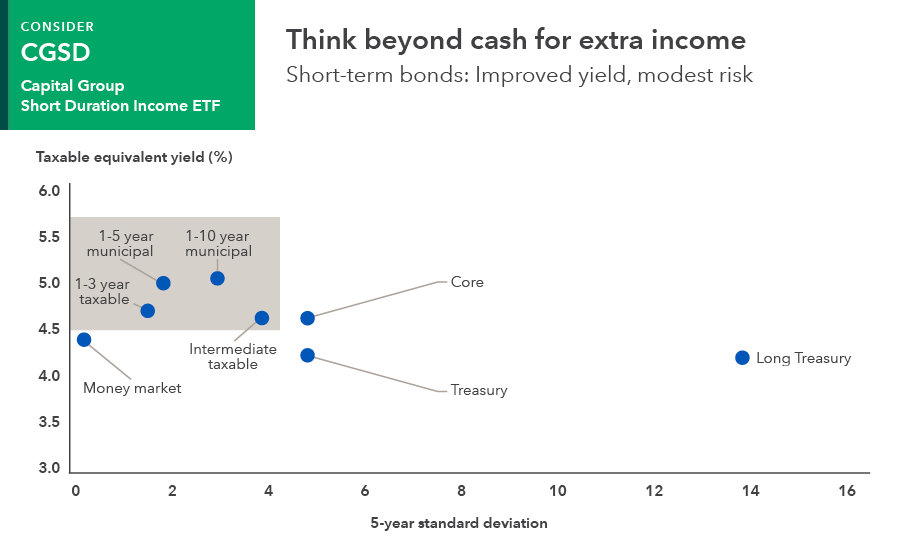

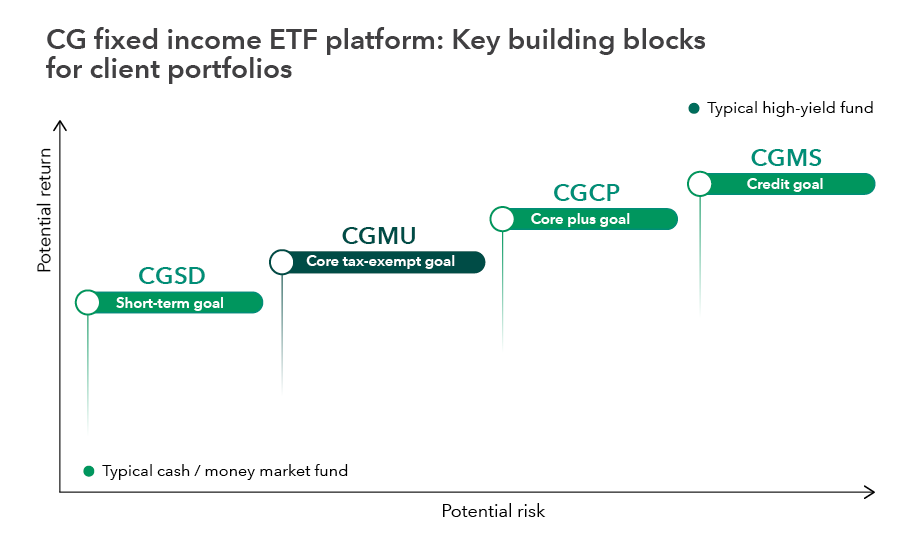

"CGSD, our short duration income ETF, has relatively low interest rate sensitivity and aims for income and capital preservation. In comparison to other short duration offerings that are income oriented, CGSD emphasizes higher quality as well as more diversity in the income-producing sectors reflected in the portfolio. We believe that may lead to less volatility over time while still delivering attractive income and returns relative to much of the yield-focused peer group."

Anmol Sinha

Investment Director for CGSD

As of December 30, 2022. Source: Bloomberg Index Services, Ltd., Morningstar. Money Market: Morningstar Prime Money Market Category average. 1-3 year taxable: Bloomberg U.S. Aggregate 1-3 Year Index, Intermediate taxable: Bloomberg U.S. Aggregate Intermediate Index, 1-5 year municipal: Bloomberg Municipal Short 1-5 year Index, 1-10 year municipal: Bloomberg Municipal Short-Intermediate 1-10 year Index, Core: Bloomberg U.S. Aggregate Index, Treasury: Bloomberg U.S. Treasury Index, Long Treasury: Bloomberg U.S. Long Treasury Index. Yields for indexes are yield to worst. Money market yield is 7-day SEC yield. Taxable-equivalent-rate assumptions are based on a federal marginal tax rate of 37%, the top 2022 rate. In addition, we have applied the 3.8% Medicare tax. Standard deviation is a common measure of absolute volatility that tells how returns over time have varied from the mean. A lower number signifies lower volatility. Past results are not predictive of results in future periods. The indexes are unmanaged and therefore, have no expenses. Investors cannot invest directly in an index.

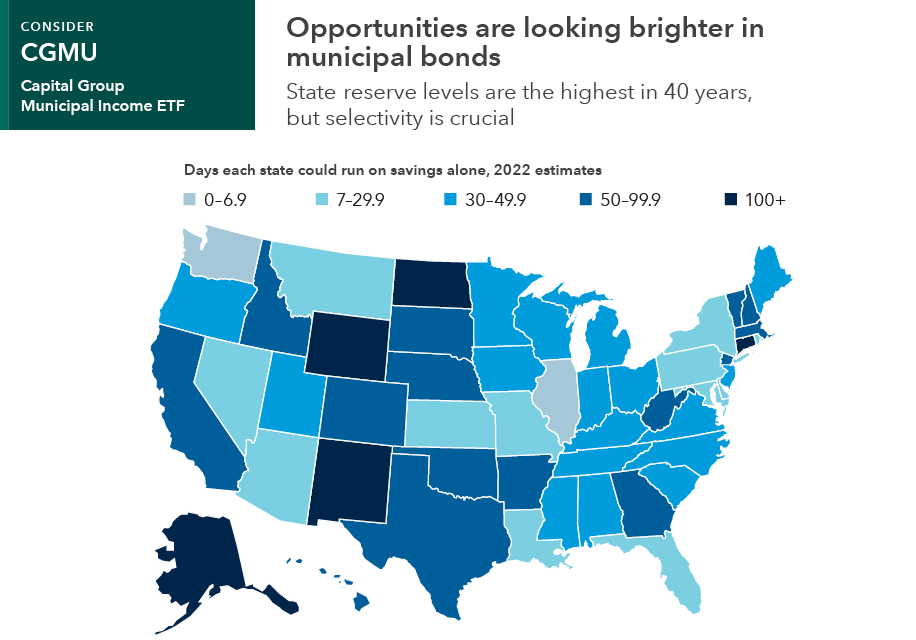

"CGMU has the flexibility to act on what managers believe could be potential weaknesses in municipal credit spreads that may pop up to create attractive valuations."

Greg Ortman

Investment Director for CGMU

Sources: Capital Group, Pew Charitable Trusts; National Association of State Budget Officers. Data is reported by each state for its fiscal year, which ends June 30 in all but four states: New York (March 31), Texas (August 31), Alabama (September 30) and Michigan (September 30).

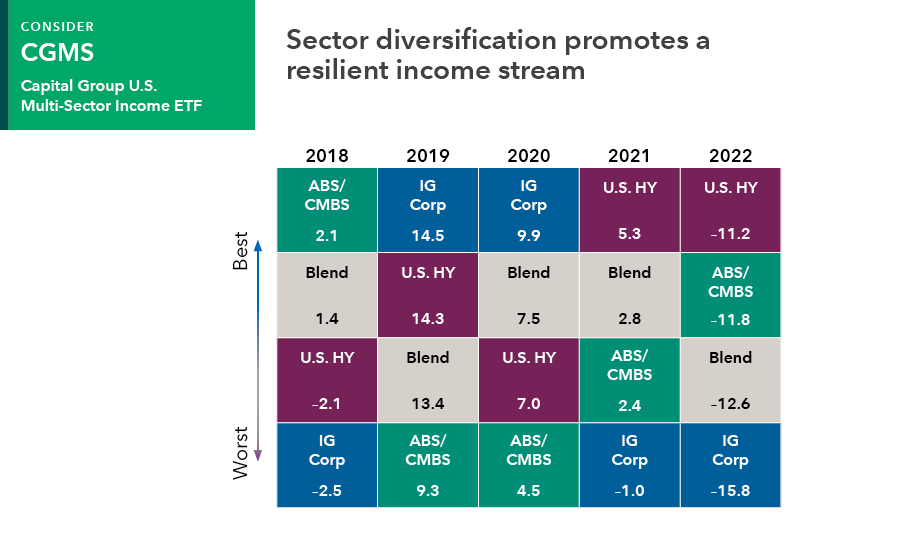

In the current bond environment, it’s important to be selective about sources of income, which is where an experienced active manager can help, particularly with a multi-sector income strategy. Such strategies allow flexibility across sectors to help focus on areas that have potential to offer the most added value.

"When pursuing higher income, you want a diversified fund for two reasons: first, diversification offers the potential for better risk management and second, no single income sector always comes out on top — therefore flexibility is a key to uncovering the best relative value across sectors and maximizing longer term risk-adjusted results. Given the complexities of credit markets, you'll want an active manager to be pulling those risk levels for you."

Harry Phinney

Investment Director for CGMS

Data as of December 31, 2022. U.S. HY represents Bloomberg U.S. Corporate High Yield 2% Issuer Capped Index; IG Corp represents Bloomberg U.S. Corporate Investment Grade Index; ABS/CMBS represents 80% Bloomberg CMBS Ex AAA Index/20%Bloomberg ABS Ex AAA Index. Blend is Multi-Sector Income Fund Custom Blended Index comprises: 45% Bloomberg U.S. Corporate High Yield 2% Issuer Capped Index, 30% Bloomberg U.S. Corporate Investment Grade Index, 15% J.P. Morgan EMBI Global Diversified Index, 8% Bloomberg CMBS Ex AAA Index, 2% Bloomberg Ex AAA Index. Past results are not predictive of results in future periods. The indexes are unmanaged and therefore, have no expenses. Investors cannot invest directly in an index.

Active fixed income management may hold added appeal in an uncertain environment

The current fixed income environment presents opportunities that may help position portfolios for the year ahead. However, if you hold passive fixed income strategies, it’s important to remember that you will need to carefully monitor interest rate risk and duration across those funds. For support in these areas, consider investing in active fixed income funds, particularly active fixed income ETFs, which may offer additional liquidity, transparency and tax benefits. Our portfolio construction team has experience identifying opportunities to simplify fixed income allocations, potentially lowering clients’ fees and allowing you to spend more time supporting your clients and growing your business. To learn more, request a consultation today.

The typical cash/money market fund and the typical high-yield fund are for illustrative purposes only and are not plotted to an index.

*Interest rate risk is the risk of a decline in the value of fixed income assets due to a change in interest rates.

†The Internal Revenue Service's wash-sale rule regulates the timing around how quickly a substantially identical security can be purchased after the underperforming asset was sold to realize a tax benefit from tax-loss harvesting.

The S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.