Midyear Outlook: From doom and gloom — to zoom and consume

August 4, 2021

There are many reasons for RIAs to be optimistic about the second half of 2021. The global recovery from the COVID-19 pandemic has gained strength, and equity and fixed income markets continue to present interesting investment opportunities. But several important headwinds remain, including investors’ increasing concerns about inflation.

We present several themes from Capital Group’s Midyear Outlook across the macroeconomic environment as well as equity and fixed income markets. We also provide RIAs with actionable steps they can consider taking to improve portfolio construction and optimize their client relationships in the second half of the year and beyond.

What a difference a year makes. A confluence of favorable events continues to unleash consumer demand and optimism, fueling the global economic recovery. Feelings of doom and gloom 12 months ago have quickly transitioned to themes like zoom and consume, as government support and the efficacy of vaccines has opened the door to a return of normal. The International Monetary Fund (IMF) is now projecting a U.S. GDP growth of 7.0% in 2021, more than double its estimate just six months ago.1

Despite this progress, many RIAs may feel like they have more questions than answers for their clients. The path to continued growth faces several apparent headwinds, including mounting concerns about inflation and interest rates. Will the U.S. Federal Reserve act sooner than expected to cool off a hot economy? Or is spiking inflation just a temporary blip on the economic radar?

We summarize key themes of Capital Group’s Midyear Outlook, including views on opportunities across equity and fixed income markets. We also provide our perspective on how RIAs can put these themes into action for their clients and further establish themselves as trusted advisors.

Inflation: Focus on CPI-YOU more than CPI-U

A reawakening of the U.S. economy — boosted by pent-up demand and unprecedented government stimulus — has led to investor fears of higher inflation. But those fears may be overblown amid ongoing weakness in the labor market and the slowing pace of vaccinations.

Despite higher prices for some raw materials and unprecedented government stimulus — has led to investor fears of higher inflation. But those fears may be overblown amid ongoing weakness in the labor market and the slowing pace of vaccinations.

Despite higher prices for some raw materials and consumer products, signs of broader price inflation appear to be short-term in nature and not the type of sustained, long-term inflation pressure that might prompt the Federal Reserve to reconsider its pledge to keep interest rates low. “Inflation should spike in the near term as stimulus-induced demand meets COVID-restricted supply,” says Capital Group economist Darrell Spence. “This is the process of the U.S. economy trying to find a new equilibrium. As stimulus wanes and the economy fully reopens, inflation should return to pre-pandemic levels of around 2% annualized.”

Inflation fears go hand-in-hand with fears of interest rate hikes. Both are exaggerated in the view of Capital Group’s rates team. Market jitters over short-term inflationary pressures have accelerated expectations for a rate increase to 2022. “That’s likely earlier than anticipated given the Fed’s stated desire to let inflation run hot and get the U.S. economy back to full employment,” says Pramod Atluri, a portfolio manager with The Bond Fund of America®.

Capital Group’s interest rates team expects the Fed to take four actions before launching its first hike since 2018. This process will likely take time, and Fed officials have made it clear that they are not in a hurry. We believe that a rate hike is probably at least 18 months away.

Four expected Fed actions before a rate increase

When considering the impacts of inflation, it can be helpful to put yourself in each individual client’s shoes. Perhaps more important than CPI-U (the Consumer Price Index for All Urban Consumers) is the idea of “CPI-YOU” — a focus on how inflation affects each individual and family differently based on their unique goals and circumstances. For example, inflation is likely a much different experience for a newly retired couple who is heavily reliant on fixed income versus a young working professional seeking to build wealth and savings. Be prepared to discuss the nuances of how inflation and the macro environment affect each individual differently.

Key takeaway:Do some extra homework for client meetings in 2021. Prepare for your client conversations with the understanding that each family is likely to have a unique, personal experience with inflation and the broader market environment. By taking a customized approach to each client, you can elevate your reputation as a trusted advisor.

Global equities: Value or growth? Balance them both

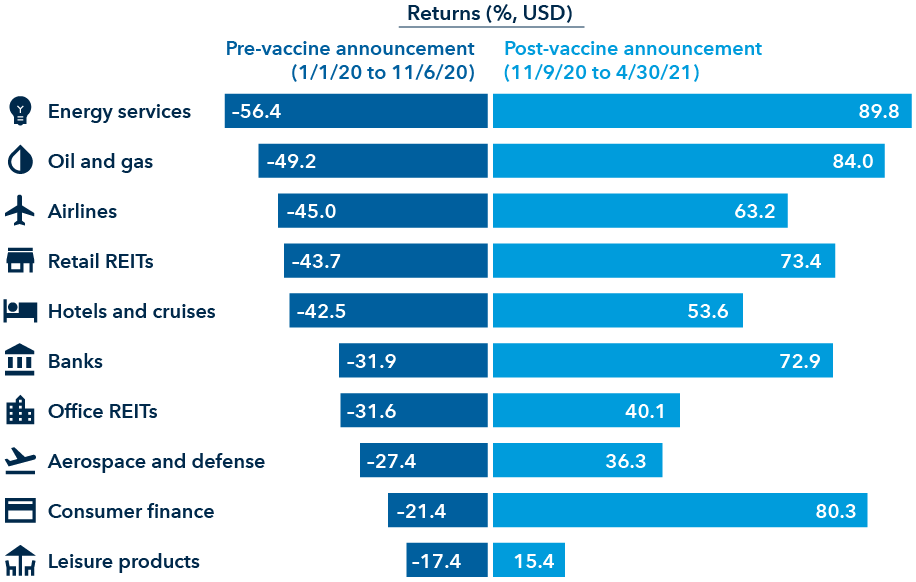

Value stocks received their own shot in the arm on “vaccine day.” After the news on November 9, 2020, that a COVID-19 vaccine was found to be highly effective, many of the industries that suffered the most during the pandemic — including airlines, hotels and commercial real estate — enjoyed strong rebounds.

Rotation to cyclicals began on November 9, or “vaccine day”

Sources: RIMES, Standard & Poor’s. Industries listed are the 10 worst performing industries within the S&P 500 Index from 1/1/20–11/6/20. Returns are in USD. 11/6/20 was the last business day before the Pfizer-BioNTech COVID-19 vaccine was revealed to have more than 90% efficacy in global trials.

So, is it time to shift from growth to value stocks? Not so fast. “There can be growing companies that are cheap and cheap companies that grow, so value and growth are not in opposition,” says equity portfolio manager Martin Romo. “We are in a target-rich environment with opportunities to invest in companies that are rapidly growing as well as classic cyclicals.”

The pandemic forced a range of behavioral changes for consumers and companies alike. “Traditional, old-economy businesses and fast-growing digital ones are using the pandemic as an opportunity to adapt by using data, technology and analytics to build a much stronger competitive position,” added Romo. The market’s perception of a company is dynamic. It may be beneficial, therefore, to take a diversified and flexible global approach to equity investing as well.

Key takeaway: Articulate your growth vs. value philosophy. Be prepared to clearly explain to clients how your firm defines growth vs. value, your views on each style of investing and how those views are reflected in clients’ portfolios.

Fixed income: Consider a framework of “core and explore”

When yields rise, the value of bonds generally declines. So, it isn’t terribly surprising that many investors are concerned about bond math today. But for investors seeking resilience, taking a longer term view and staying the course with core bonds still could make sense. While the past is not a predictor of future results, during the five sharpest 10-year yield spikes over the past three decades, the total core bond return remained positive from when yields were lowest before those increases to two years later.2

Whether bond yields rise or fall, a strong core allocation should seek to deliver the four roles of fixed income: capital preservation, inflation protection, income, and diversification from equities. The core benchmark’s average three-year correlation to the S&P 500 Index since 1975 has been 0.16.3 This suggests a level of potential diversification that may be beneficial if there are setbacks on the road to recovery.

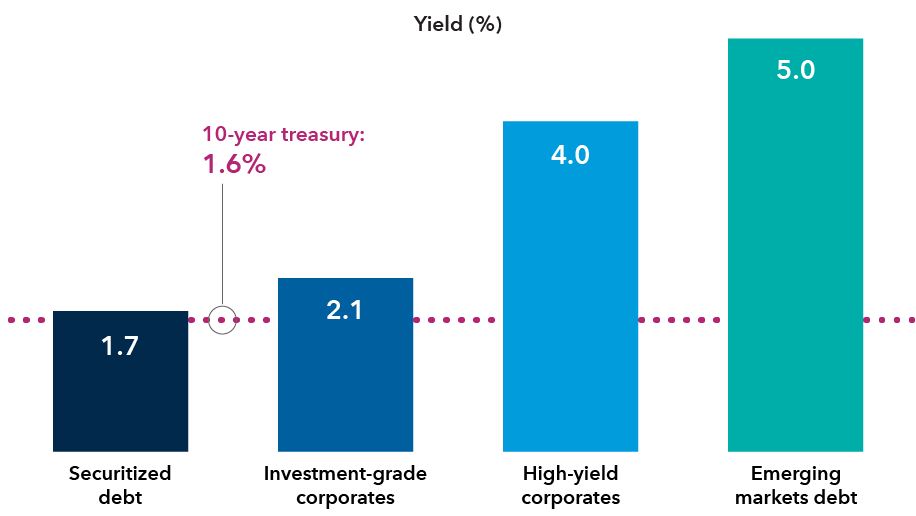

Looking beyond the core, it may be a good time to diversify your bond portfolio. Corporate default rates should continue to fall as consumers put money to work buying goods and services. Fewer defaults may provide a boost to corporate bonds, particularly those in the high-yield sector. However, it could also tempt investors to take on greater risk, especially as interest rates remain near historic lows.

Exposure to emerging markets bonds and securitized debt can also help support income needs. By blending higher income sectors, investors can potentially capture more yield and reduce the overall volatility of their portfolios.

Consider opportunities across higher yielding fixed income sectors

Sources: Bloomberg Index Services Ltd., Refinitiv Datastream, RIMES, J.P. Morgan. As of 5/31/21. Bloomberg Barclays U.S. Securitized Index represents the universe of mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities. Bloomberg Barclays U.S. Corporate Investment Grade Index represents the universe of investment grade, publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. Bloomberg Barclays U.S. Corporate High Yield Index covers the universe of fixed-rate, non-investment-grade debt. J.P. Morgan Emerging Market Bond Index (EMBI) Global Diversified is a uniquely weighted emerging market debt benchmark that tracks total returns for U.S. dollar-denominated bonds issued by emerging market sovereign and quasi-sovereign entities.

Credit selection is key in the higher yielding sectors of fixed income, as long-term fundamentals can be challenging, particularly for many low-quality issuers. The global diversity in emerging markets bonds today also calls for deep credit analysis. Understanding why a specific bond pays a higher yield can help investors determine which bonds may provide durable, long-term income.

Key takeaway: Go active when searching for yield. When searching beyond the core for higher yielding fixed income opportunities, it may make sense to emphasize active management due to the more esoteric nature of asset classes like high-yield bonds and emerging markets debt.

Capital Group insight: Focus on thought leadership in the second half of 2021

Despite reasons for cautious optimism, many of your clients may still feel uncertain about the future and uneasy about some aspects of their financial lives. In this type of environment, RIAs can make a meaningful impact by focusing more attention on client communications and thought leadership.

But many advisors may lack the time or resources to produce valuable thought leadership content for clients. Capital Group’s Marketing Lab can help. Marketing Lab makes it easy for advisors to stay connected with their clients through personalized, professional-looking thought leadership emails and social media posts — all customized for your firm. Learn more or get started today.

1 Source: Reuters, “IMF raises U.S. 2021 growth forecast to 7%,” July 1, 2021

2 Sources: Capital Group, Bloomberg Index Services Ltd., Federal Reserve Bank of St. Louis. Periods were determined by considering the 10-year Treasury constant maturity rate measured daily over the 30 years ending 5/15/2021. Yield increase period end dates are: 11/7/1994, 1/20/2000, 6/10/2009, 12/31/2013 and 7/5/1996, respectively.

3 Average three-year correlation calculated monthly from the inception of the Bloomberg Barclays U.S. Aggregate Index, 12/31/1975 through 5/31/2021. Bloomberg Barclays U.S. Aggregate Index represents the U.S. investment-grade fixed-rate bond market.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Lower rated bonds are subject to greater fluctuations in value and risk of loss of income and principal than higher rated bonds.

The return of principal for bond portfolios and for portfolios with significant underlying bond holdings is not guaranteed. Investments are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings.

There have been periods when the results lagged the index(es) and/or average(s).

The indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

This report, and any product, index or fund referred to herein, is not sponsored, endorsed or promoted in any way by J.P. Morgan or any of its affiliates who provide no warranties whatsoever, express or implied, and shall have no liability to any prospective investor, in connection with this report. J.P. Morgan disclaimer: https://www.jpmm.com/research/disclosures

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.

For financial professionals only. Not for use with the public.